Frothy Sentiment Rides Bullish Technicals

The post-election environment and positive developments toward a COVID-19 vaccine have led to a surge in stock prices. The added clarity on these two fronts has boosted sentiment, which may present a risk in the near term as stock prices are near all-time highs.

A November to Remember

The reaction from stocks since the US election has been truly impressive. The S&P 500 Index is up 8.8% for the month, on pace to be the best November for the S&P 500 in 40 years. Small caps have also soared, with the Russell 2000 Index up 16%, which would be its second-best month ever. Although we remain longer-term bullish on equities, there are some signs that sentiment could be getting a little frothy at the moment, which could increase the odds of a pullback.

Technicals Supportive of Future Strength

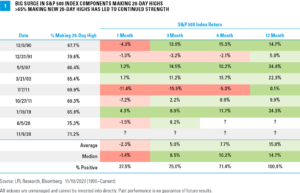

On November 9, more than 71% of the stocks in the S&P 500 hit a one-month high, the third-highest reading using data back to 1990. Not only does this tell us that participation in the post-election rally has been extremely broad and not limited to only a few heavily weighted names in the index, but historically this has been an extremely positive signal for the next year. Returns can be quite weak in the near term after more than 65% of stocks reach a one-month high, but returns over the next 12 months not only have been far above average, but have been positive in all seven observed instances [Figure 1].

In fact, nearly every measure of breadth and participation we monitor shows a similar trend. Looking at longer-term indicators, 90% of the stocks in the S&P 500 are above their respective 200-day moving averages—a common method of identifying stocks in uptrends. Readings above 85% have signaled above-average forward returns over the next 6 and 12 months.

Finally, participation has not been limited simply to large cap stocks. After lagging the S&P 500 by more than 16% in the first quarter of 2020, last week the small cap Russell 2000 Index made its first record high in more than two years and is now outperforming the S&P 500 by 11% thus far in the fourth quarter.

Could Sentiment be Flashing a Warning?

Given that the S&P 500 was down more than 30% for the year at the March 2020 low, it is perfectly normal to sense some excitement in the air as stocks have climbed back to new all-time highs. “Nothing changes sentiment like price” is an old saying; however, excessive optimism can open the door for contrarian sellers to weigh on prices. When we upgraded our view on equities to overweight in late March 2020, one of the main reasons was the overriding sentiment backdrop of extreme pessimism that left limited opportunity for further selling. Any good news likely could have sparked a major rally, and as the economy has continued to surprise to the upside, that’s exactly what we have seen since the March lows.

We would view any pullback or correction as an opportunity to add equity exposure; however, we also see some potential near-term warning signs that may open the door to weakness.

- Sentiment polls. The American Association of Individual Investors (AAII) Sentiment Survey recently had 55.8% bulls, the highest number of bulls since January 2018. Bulls also had their largest one-week jump in 10 years. Meanwhile, the Investors Intelligence US Advisors’ Sentiment Report saw the number of bulls move to 59.6%, just below the extreme level of 60% and a three-year high. The last time bulls were this high was in late August 2020, right before a nearly 10% correction in the S&P 500.

- Flows. Investors have quickly moved back into equities as well. According to EPFR Global, global equity funds saw inflows of nearly $45 billion the week after the 2020 election in November, the largest inflow in nearly 20 years of data. US stock funds added $33 billion, the second most for one week. Over the past two weeks, global flows have hit a record $71 billion as well. The Bank of America Global Fund Manager Survey samples 190 fund managers with more than $526 billion in assets, and the recent survey showed global growth and profit optimism at a 20-year high. Cash positions fell to pre-Covid-19 levels, while allocation to equities is the highest it has been since January 2018 and near extreme bullish levels (great than 50%).

- Put/Call ratios. Another potential contrarian warning can be found in the options market. The 10-day moving average of the Chicago Board Options Exchange (CBOE) put/call ratio is in the 91st percentile, suggesting a good deal of optimism from option traders.

Where Do We Go From Here?

Markets have certainly been on a wild ride in 2020, and there’s a degree of irony when you consider that we’re talking about overconfidence by investors in a year that had the fastest bear market in history. However, while frothy sentiment gauges are suggestive of caution in the near term, the underlying technical data is suggestive of positive returns over longer time horizons. We continue to remain overweight equities in our models and view pullbacks as a buying opportunity for investors who may want to consider adding exposure.

Read previous editions of Weekly Market Commentary on lpl.com at News & Media.

Ryan Detrick, CMT, Chief Market Strategist, LPL Financial

Scott Brown, CMT, Senior Analyst, LPL Financial

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

Please read the full Midyear Outlook 2020: The Trail to Recovery publication for additional description and disclosure.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-29754-1120 | For Public Use | Tracking # 1-05082119 (Exp. 11/21)