Corporate America has capped off an outstanding 2021 with an excellent fourth quarter earnings season so far. Entering 2021, the consensus estimate for S&P 500 Index earnings per share (EPS) was less than $170. Now with fourth quarter results mostly in the books, that number is 22% higher at $208. Here we recap another solid fourth quarter earnings season and discuss what the results could mean for earnings growth and stock market performance in 2022.

Delayed Investor Shift From Macro to Micro

In our earnings preview on January 10, we noted that we welcomed a shift from the macro to the micro. Well, given the path of inflation, the resulting dramatic shift in Federal Reserve (Fed) rate hike expectations, and the escalating Russia-Ukraine conflict, that shift hasn’t really happened. However, when we turn our attention away from macro headlines to corporate America, we find that companies have again showcased their ability to effectively manage through the pandemic’s challenges, notably supply chain disruptions and labor and materials shortages that have pushed costs higher.

Great Numbers

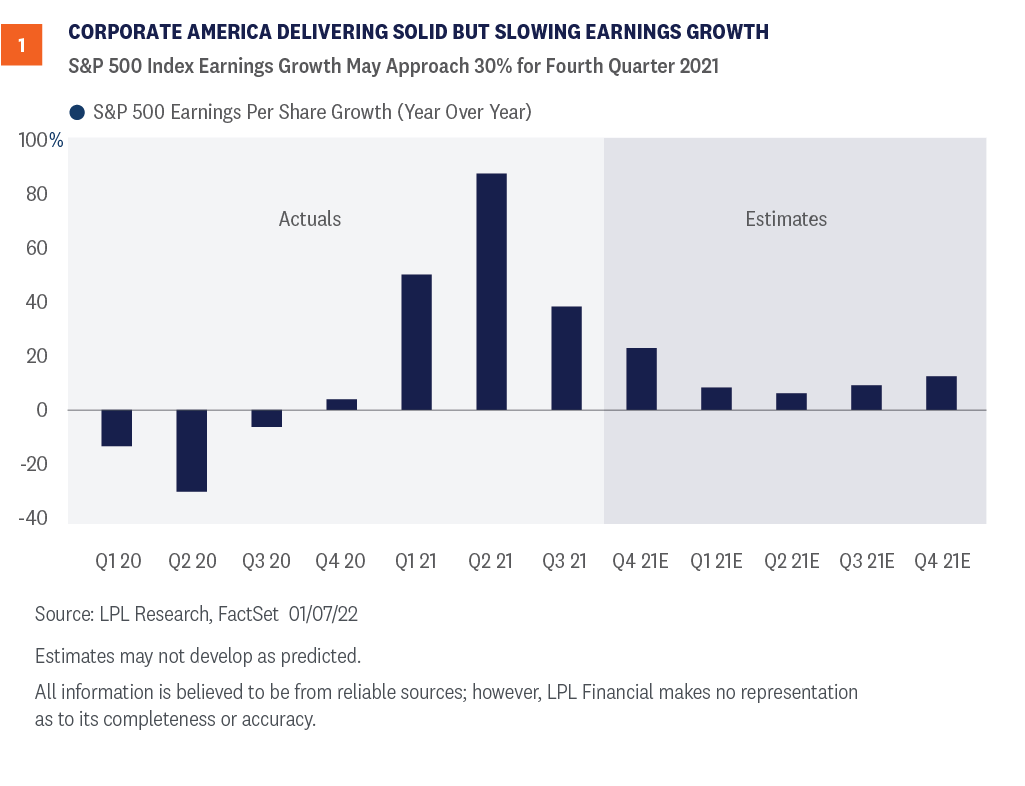

The numbers this earnings season have been great even without considering that the bar has been raised consistently throughout the pandemic. S&P 500 earnings per share are tracking to a 31% year-over-year increase, shown in [Figure 1], roughly 10 percentage points above the consensus estimate when earnings season began. That upside will likely fall a bit short of the 12 points of upside in the third quarter, but considering the long-term average upside is about five percentage points, and the fourth quarter was wrought with pandemic-related challenges, we’re quite impressed. In fact, in our earnings preview last month, we wrote, “Earnings growth approaching 30%, though slower than the third quarter’s near-40% clip, would be impressive given the challenging operating environment.”

How Have They Done It?

Though about 75 S&P 500 companies have yet to report, companies have generally beaten estimates soundly again with a combination of surprising revenue strength and resilient profit margins. Fourth quarter 2021 revenue came in about three percentage points above consensus estimates at more than 15.5%, bolstered by the strong economic growth in the quarter (6.9% real gross domestic product growth annualized), fueled by inventory restocking, as well as price increases. That 15.5% revenue growth is higher than any quarter during the previous economic expansion (2009-2020), but was bested by the second and third quarters of 2021 that saw growth inflated by base effects coming off 2020 lockdowns. This solid revenue upside, which is about twice the long-term average “beat”, came despite supply chain disruptions limiting what companies had available on the shelves to sell, labor shortages that cost companies sales they otherwise would have booked, and the COVID-19 Omicron wave in late November through December that constrained economic activity. The other part of the earnings story is the impressive profit margins. Due to rising costs of labor, materials, energy, and transportation, we had anticipated some meaningful profit margin compression in the quarter. It looks like we’ll end up with a slight downtick in margins quarter over quarter when all the results are in, but it won’t be as big of a drop as we had feared. That slight potential dip from the third quarter to the fourth doesn’t take away from the fact that margins last year were tremendous [Figure 2]. Companies are enjoying pricing power, which is helping them pass along higher costs, notably wages, and largely preserve those high margins that are well above pre-pandemic levels.

Carrying Earnings Momentum Into 2022

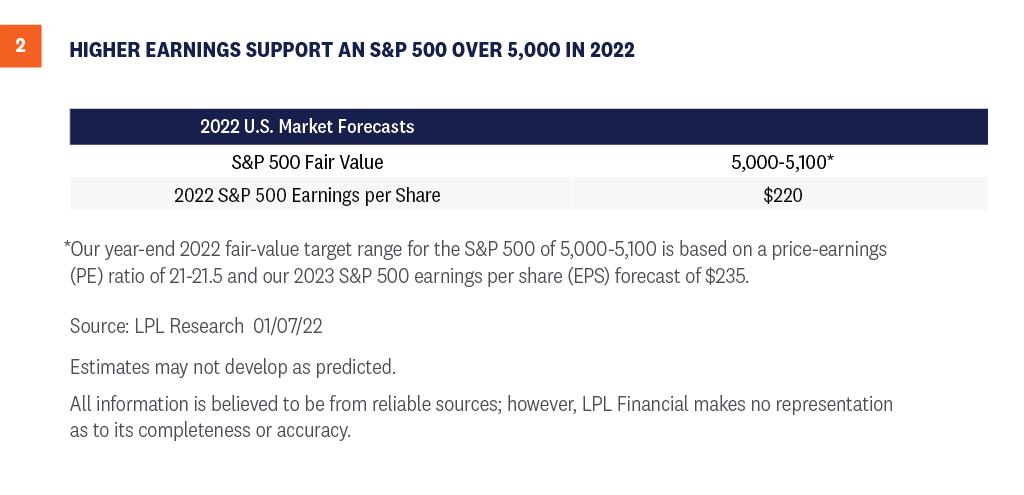

We remain concerned about higher wages and other inflation pressures crimping margins in 2022. Supply chain challenges will likely linger through the first half of the year based on commentary from a number of companies in recent weeks. Still, the impressive profitability displayed in the fourth quarter puts corporate America in a strong position to potentially deliver higher earnings in 2022 than we previously anticipated. On the revenue side, remember higher prices translate into more sales, as long as demand remains strong enough to pay those higher prices. Pricing power helped companies in the fourth quarter and should continue to help in 2022. If the U.S. economy grows near our 4% forecast in real terms this year, adjusted for inflation, and consumer inflation adds another five points (consensus forecast of economists according to Bloomberg), then we believe 9% revenue growth from S&P 500 companies is a reasonable expectation. For perspective, the best revenue growth years since the 2008-2009 financial crisis were 2011 (+12.5%) and 2021 (+16.9%). That means our 6-7% earnings growth forecast for 2022 could be attainable even with modest margin compression (with some help from share repurchases reducing the denominator in the earnings-per-share calculation). For now, we’ll maintain our forecast of $220 in S&P 500 EPS in 2022, but that number could be too low based on the earnings momentum evident this earnings season. The consensus estimate for 2022 S&P 500 EPS rose 0.5% during earnings season, much better than the average 2-3% reduction observed historically.

Macro Backdrop Still Supports 5,000 on the S&P 500 at Year End

Stocks have gotten off to a rough start this year. The adjustments to higher inflation and more Fed rate hikes have been difficult, while the Russia-Ukraine situation has added to market anxiety and volatility. While it may take more time for the market to shift its focus toward solid company fundamentals and get more comfortable with the inflation outlook, we expect stocks to recover early-year losses and rally back to new highs through year-end as that transition takes place. Mid-cycle years such as 2022 tend to see double-digit gains for stocks, even more optimistic than the high-single-digit gain we forecasted in our Outlook 2022: Passing the Baton. History shows that stocks tend to do well during the year after initial Fed rate hikes and that volatility related to geopolitical events has frequently been short-lived. The additional reopening of the economy that lies ahead makes solid growth in the U.S. economy and corporate profits, in our opinion, more likely this year and should help ease inflation pressures, solidifying a favorable backdrop for attractive stock market returns in 2022. The recent move higher in interest rates doesn’t change the calculus much for us in terms of stocks versus bonds. We continue to recommend an overweight allocation to equities and an underweight fixed income allocation relative to investors’ targets, as appropriate. Jeff Buchbinder, CFA, Chief Equity Strategist, LPL Financial Ryan Detrick, CMT, Chief Market Strategist, LPL Financial ______________________________________________________________________________________________ IMPORTANT DISCLOSURES This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy. U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio. All index data from FactSet. This research material has been prepared by LPL Financial LLC. Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity. Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-1056300-0222 | For Public Use | Tracking # 1-05246331 (Exp. 2/23)

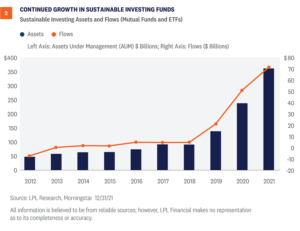

Sustainable investing hit several milestones in 2021, but continued to attract its critics. Below we look at how sustainable investing fits within the broader concept of sustainability, its growth during 2021, and an implementation framework that has been helpful for many. A well diversified sustainable investing portfolio doesn’t mean that an investor has to make a choice between achieving market-like returns and being an aware social and environmental steward. Market volatility has been the dominant story for many investors in early 2022, but even as we focus on near term events it’s important to continue to track important market trends. Sustainable investing has become a significant theme in how many investors choose to direct some or all of their capital, choosing to emphasize businesses that show they’re in it for the long term. The space has been evolving as it continues to meet its critics and address the challenges that come with growth, with several important developments in 2021.

What is Sustainability?

The concept of sustainability can easily get bogged down in confusing definitions and minutia. Most simply, sustainability is humanity meeting its current needs without overburdening the natural environment or future generations. Environmental sustainability refers to maintaining the balance of natural systems and that natural resources are consumed at a rate that can be replenished. Social sustainability refers to a minimum standard of basic necessities and that human rights is afforded to all people. As shown below, sustainability includes action by individuals, companies, governments, and increasingly investors. Environmental, social, and governance (ESG) issues fit within sustainability, but in its broadest sense ESG is a grading system for firms. ESG criteria are used by investors to gauge companies (and increasingly governments) on their ESG performance relative to their peers. Environmental metrics may include a company’s carbon dioxide emissions, water usage, or impact on deforestation. Social metrics may include a company’s employee engagement, diversity and inclusion, and employee health and safety. Governance metrics may include a company’s board composition, executive compensation, and other internal procedures. Sustainable investing incorporates ESG metrics into the investment process to provide greater transparency and help manage ESG risks and opportunities. As illustrated in [Figure 1], sustainable investing is part of a larger effort to provide social and environmental awareness and stewardship.

Growth of Sustainable Investing

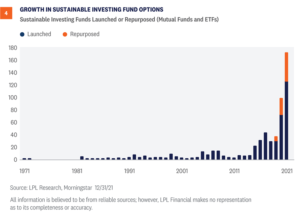

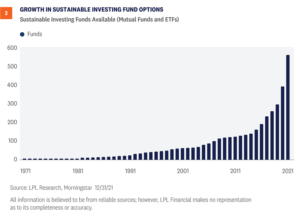

Sustainable investing mutual funds and exchange-traded funds (ETFs) continue to attract record flows from investors [Figure 2]. Determining this universe involves the identification of funds that demonstrate a commitment to ESG considerations in their investment process (disclosed in the principal investment strategies section of their prospectus). As of December 31, 2021, assets grew 52% from the year before to $362 billion. The universe of sustainable investing mutual funds and ETFs has also continued to grow since the first fund was launched in 1971 [Figure 3]. The growth in available options provides investors with a spectrum of choices, from being able to build a diversified stock and bond portfolio, to selecting a specialized strategy to supplement a traditional diversified portfolio. In 2021, the number of available choices grew 44% to 560. As a wider range of investors continue to incorporate sustainable investing in their investment process, there’s been a growing trend of traditional investment strategies being repurposed as sustainable investing strategies [Figure 4]. During 2021, 45 funds were repurposed while 125 funds were launched. The implication for investors is the need to thoroughly vet strategies to ensure the investment is delivering on the claims made in its supporting literature.

How to Implement Sustainable Investing Strategies

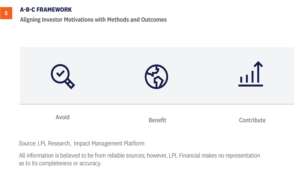

Sustainable investing is not a one-size-fits-all approach as interest varies by investor. For investors, the place to start is to understand their own motivations for their interest in sustainable investing. Motivations for sustainable investing are often grouped into values alignment, financial performance, and impact. Once motivations are clear, they can then be mapped to one or all of the outcomes described below. Finding a strategy or two, becoming more aware of various approaches, and slowly increasing one’s exposure to sustainable investing is a common way to get started.

Act to Avoid Harm: Values Alignment

Example: investors can signal that responsible corporate behavior matters.

“I don’t want to support companies that harm the environment, violate human rights, or engage in unfair labor practices.”

Motivation: some investors are motivated by the awareness that their investments should be transparent and align with responsible behavior, consistent with their approach to consumption. Investing method: negative/exclusionary screening – a process that excludes investment in companies, industries, or countries based on moral values and other specific standards. Outcome: periodic review to confirm investment portfolio does not contain previously agreed upon companies, industries, or countries.

Benefit Stakeholders: Financial Performance

Example: investors can engage actively to improve ESG performance of companies.

“I want companies to have a positive effect on society.”

Motivation: some investors see sustainable investing as a way to unlock commercial value, such as backing companies with strong ESG practices that are better positioned to adapt to a changing world. Investing method: ESG integration – intentionally consider the role of ESG factors in building a strong business alongside traditional financial analysis to identify ESG risks and opportunities. Outcome: periodic review to confirm investment portfolio has lower exposure to certain ESG risks, such as greenhouse gas emissions, or higher exposure to certain ESG opportunities, such as alternative energy solutions.

Contribute to Solutions: Impact

Example: investors can supply capital to underserved communities.

“I want to help tackle the affordable housing gap.”

Motivation: some investors are motivated to create positive change. Investing method: impact investing – investments made with the intention to generate social and environmental impact alongside a financial return. Outcome: periodic review to confirm assets channeled to underserved community are leading to tangible impacts. The above process is known as the A-B-C Framework (avoid, benefit, contribute), which may help align investors’ motivations, investment methods, and expected outcomes. Jason Hoody, CFA, Head of Investment Manager Research & Sustainable Investing Research, LPL Financial ______________________________________________________________________________________________ IMPORTANT DISCLOSURES This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy. An Environmental, Social and Governance (ESG) fund’s policy could cause it to perform differently compared to funds that do not have such a policy. The application of social and environmental standards may affect a fund’s exposure to certain issuers, industries, sectors, and factors that may impact relative financial performance — positively or negatively — depending on whether such investments are in or out of favor. U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio. All index data from FactSet. This research material has been prepared by LPL Financial LLC. Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity. Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-1023100-0122 | For Public Use | Tracking # 1-05238004 (Exp. 1/23)

Corporate America has been on quite a run. Coming into 2021, S&P 500 Index companies were expected to generate less than $170 in earnings per share. As 2022 begins, it looks like that number may end up higher than the latest LPL Research estimate of $205, one of the biggest earnings upside surprises ever and a big reason why stocks did so well last year. But 2021 earnings are not yet fully in the books. We have one more quarter to go, which we preview here.

Big banks kick us off

Fourth quarter earnings season kicks off this week with earnings from several big financials, including BlackRock, Citigroup, JPMorgan Chase, and Wells Fargo reporting on Friday, January 14. This week just seven S&P 500 constituents report, but another 40 will announce results the following week (January 17-21) and 99 the week after that (January 24-28). We welcome the shift from the macro to the micro where companies can continue to showcase their ability to effectively manage through the pandemic challenges, notably the supply chain disruptions and labor and materials shortages that are pushing costs higher.

What to expect

We expect another good earnings season overall in which companies continue to beat expectations in aggregate and produce solid growth. Consensus estimates are calling for a year-over-year increase in S&P 500 earnings in the fourth quarter of about 22% [Figure 1]. The long-term average upside surprise of around five percentage points makes 27% a reasonable target, but given earnings beat estimates by 12 percentage points last quarter, the number could be higher. Earnings growth approaching 30%, though slower than the third quarter’s nearly 40% clip, would be impressive given the challenging operating environment. We see several reasons to remain optimistic for this earnings season. First, estimates have been rising. Since the end of October 2021, the consensus estimate for fourth quarter S&P 500 EPS has increased 3.3%. Second, manufacturing activity has remained healthy based on purchasing managers’ surveys—the U.S. Institute for Supply Management (ISM) manufacturing index averaged a very strong 60.2 in the fourth quarter— in both the headline number and the new orders component. Additionally, in the December report there were signs of lower input prices and some easing of supply chain disruptions. Third, we expect the COVID-19 Omicron variant to have limited impact on demand, i.e., revenue, in the quarter. The Bloomberg-tracked consensus forecast for gross domestic product (GDP) growth in the fourth quarter is 5.2% year over year. Add a consumer price index (CPI) increase of over 6% year over year and it’s easy to see how 12.7% revenue growth, the current consensus, is possible. Remember, higher prices end up as more revenue for someone, as higher costs are passed along to customers. That’s why equities have preserved their value through inflationary periods over time. At the same time, there are some reasons to be concerned about less upside and more shortfalls. The Omicron variant did slow economic activity in December. And the ratio of negative pre-announcements to positives (1.7) has been more negative than the prior quarter’s ratio of 0.8, according to Refinitiv data.

What we’re watching

Margins, margins, margins. We will continue to watch for signs of pressure on profit margins from rising costs of labor, materials, and transportation. We came away from third quarter earnings season with the impression that most supply chain issues would be resolved by midyear. Any information contrary to that could influence the market’s response to results and direction of analysts’ earnings estimates for 2022. Wages are key. Wages are the single biggest component of companies’ costs, so we will be looking for confidence from companies that wage pressures are manageable. We anticipate higher wages will soon start to eat into profit margins, as productivity gains from technology investments (i.e., doing more with less) can only go so far. We would like to see more workers enter the labor force to help contain wage increases, which are already running above 4% annualized. Ability to pass on higher costs. We’ll also be interested to hear companies’ comments on the stickiness of price increases. If customers are starting to balk at higher prices, we may see some impact on demand and therefore revenue in coming quarters.

Earnings outlook for 2022

As we discussed in Outlook 2022: Passing the Baton, we expect a very favorable revenue environment in the coming year, with potential above-average economic growth and price increases. Revenue growth has historically been closely tied to nominal GDP growth (real “inflation–adjusted” GDP growth plus inflation). Our 4–4.5% real GDP growth forecast for next year, plus at least a few percentage points of inflation, puts 7% revenue growth in play, which is where consensus is currently. But margins are the tricky part. If they are stable—no small task—then a double-digit percentage increase in S&P 500 earnings per share (EPS) is possible. That would put S&P 500 EPS near $230 in 2022 and well above our current forecast of $220 [Figure 2]. But higher costs from COVID-19-related supply chain disruptions and materials and labor shortages are unfortunately not going away anytime soon. Wages are on the rise (average hourly earnings in Friday’s employment report rose 4.7% year over year, well above the 4.2% that was expected). And COVID-19 is still slowing economic activity. So, we prefer to be a bit more cautious for now and keep our S&P 500 EPS below-consensus forecast at $220, about 7% above our already conservative 2021 estimate of $205. We believe a continued economic expansion in 2023 as the impacts of COVID-19 fade, along with only a small potential hit from tax increases, will get us to $235 in S&P 500 EPS next year. That assumes a scaled-down version of Build Back Better with some tax increases passes. If it doesn’t, which we see as less likely, there won’t be any tax drag, introducing some upside potential to earnings next year.

Look for 5,000 on the S&P 500 in 2022

Despite the Fed’s accelerated tightening timetable, we continue to believe the S&P 500 will reach 5,000 in 2022. Earnings will have to do the heavy lifting to get us there with valuations elevated, though we believe a price-to-earnings ratio (P/E) in the 21–22 range is fair even if interest rates move modestly higher—that gets us to 5,000+ by year-end 2022. As the market continues to adjust to tighter monetary policy and factors in the still uncertain path of COVID-19, more volatility is likely. But that doesn’t change our enthusiasm for stocks here, especially relative to bonds, powered by solid earnings gains, the likelihood that COVID-19 risks fade as the year progresses, and our belief that inflation will be manageable in the latter part of this year. Jeffrey Buchbinder, CFA, Equity Strategist, LPL Financial

Ryan Detrick, CMT, Chief Market Strategist, LPL Financial

______________________________________________________________________________________________ IMPORTANT DISCLOSURES This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy. U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio. All index data from FactSet. This research material has been prepared by LPL Financial LLC. Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity. Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-1000900-0122 | For Public Use | Tracking # 1-05229974 (Exp. 1/23)

We expect solid economic and earnings growth in 2022 to help U.S. stocks deliver additional gains next year. If we are approaching—or are already in—the middle of an economic cycle with at least a few more years left (our view), then we believe the chances of another good year for stocks in 2022 are quite high. We believe the S&P 500 could be fairly valued at 5,000–5,100 at the end of 2022, based on an EPS estimate of $235 for 2023 and an index P/E between 21 and 21.5. Most of this content was taken from Outlook 2022: Passing the Baton We expect solid economic and earnings growth to help stocks deliver gains in 2022. When forecasting stock market performance, we start with the economic cycle. We believe we are currently approaching—or are already in—the middle of an economic cycle with at least a few more years left. Historically, if this holds true, then we believe the chances of another good year for stocks in 2022 are quite high, which is an important added factor for our positive outlook for stocks next year [Figure 1].

The Mid-Cycle Push

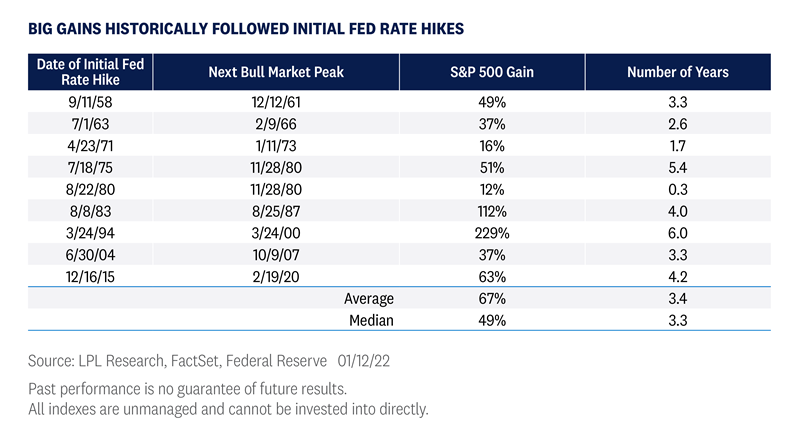

Looking more closely, in a mid-cycle economy, recession fears do not typically cause stocks to fall in a given year, nor do stocks typically surge as investors celebrate emerging from the prior recession. Over the past 60 years, the S&P 500 Index was up an average of 11.5% during the 30 mid-cycle years we identified, with gains in 80% of those years [Figure 2]. As you can see, stocks rose during most of these mid-cycle years, with 1966 and 1977 being the only two years with double-digit losses. The Fed, which we expect to start raising interest rates in early 2023, can also help us gauge the cycle because the central bank typically begins to raise rates when the economy is exhibiting mid-cycle characteristics. That also characterizes 2022 as a likely mid-cycle year. Historically, stocks have done very well during the 12 months leading up to the Fed’s initial rate hike, with gains in each of the past nine instances and an average gain of 15%. Although the timetable for the initial Fed rate hike has been moved forward several months, we expect stocks to follow this mid-cycle pattern and potentially deliver double-digit gains next year as the economy continues to expand at a solid pace.

Earnings are the Anchor

An expanding economy is a great start, but stocks fundamentally derive their value from earnings. On the top line, the environment for companies to grow revenue next year should be excellent, with potential for above-average economic growth and some pricing power from elevated inflation. Revenue growth has historically been well correlated to nominal GDP growth, which is simply real GDP growth (the inflation-adjusted number that’s normally reported) plus inflation. Our 4–4.5% real GDP growth forecast for next year plus perhaps 3% inflation (about the consensus forecast for the increase in the Consumer Price Index) puts a 7% revenue increase in play. With stable profit margins and increasing share buybacks likely next year, a double-digit percentage increase in S&P 500 earnings per share (EPS) is a possibility. But COVID-19-related supply chain issues and materials and labor shortages are risks that could lead to higher costs in 2022, potentially weighing on profit margins. Many companies warned of such pressures during third-quarter earnings season. As a result, we are forecasting slightly below-average S&P 500 earnings growth in the 6-7% range in 2022 to $220 per share. At this point it is unlikely that higher corporate taxes will eat into any of those earnings gains next year, as they have reportedly been pushed out into 2023 in negotiations for President Biden’s social spending package.

Valuations May Not Provide an Assist

Forecasting a year ahead is tough enough, but predicting where stocks might be at the end of 2022 actually requires us to look ahead to 2023. The 2023 earnings outlook will determine where valuations are likely to be at the end of 2022. Strong earnings gains in 2021 have prevented the price-to-earnings ratio (P/E) for the S&P 500 from going much above 20. In fact, stocks are actually more reasonably priced as 2022 approaches than they were at the start of 2021, because 2021 earnings are tracking more than 20% above the estimate when the year began. While a 21 P/E is above the long-term average of around 16, we believe still low interest rates justify current valuation levels. But P/E multiple expansion will likely be difficult if interest rates rise in 2022, potentially leaving earnings growth as the primary driver of any stock market gains.

S&P 500 Index Knocking on the Door of 5,000?

5,000 on the S&P 500 will be a nice round number for investors to celebrate. But will that celebration take place in 2022 or later? If we assume S&P 500 EPS growth in 2023 stays around its long-term average, implying roughly $235 in EPS, while the P/E stays about where it is between 21 and 21.5, the S&P 500 could be fairly valued at 5,000–5,100 at the end of 2022. Note, however, that stocks can stay above (or below) fair value for an extended period of time due to market sentiment, so we would not necessarily view reaching that target as a sell trigger. If interest rates stay lower for longer and support P/E multiple expansion, stocks could potentially exceed this target by year-end 2022. But if profit margins face more intense pressure than anticipated, possibly from wages, earnings may have a hard time growing at all in 2022.

The Race Continues in 2022

Prospects for above-average economic growth and accompanying earnings gains in 2022 point to another potentially good year for stock investors. While the pandemic is not completely behind us as the COVID-19 Omicron variant spreads rapidly (though with a high proportion of mild cases), and there are several other risks to watch, particularly inflation, stocks have historically done well in mid-cycle economies. We do not expect 2022 to be an exception. Ryan Detrick, CMT, Chief Market Strategist, LPL Financial

Jeff Buchbinder, CFA, Chief Equity Strategist, LPL Financial ______________________________________________________________________________________________ IMPORTANT DISCLOSURES This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy. U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio. All index data from FactSet. This research material has been prepared by LPL Financial LLC. Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity. Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-984450-1221| For Public Use | Tracking # 1-05223960 (Exp. 12/22)

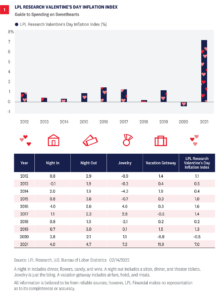

High inflation continues to cloud the economic outlook while its impact on the potential path of rate hikes has left markets unsettled. Inflation is a serious topic, but occasionally it’s useful to revisit it from a lighter perspective. Today is Valentine’s Day, and as we do every year, LPL Research takes a look at changing prices from the perspective of some popular ways to celebrate the day with our annual Valentine’s Day Index. Do you want to know what you might be paying this year for a night in, a night out, a special piece of jewelry, or even a vacation? LPL Research has you covered. Today is Valentine’s Day, a day when many celebrate romance, although the scope of the day has expanded to friendship and even just simple holiday fun. According to the National Retail Federation, Valentine’s Day ranks fourth in holiday spending, with average spending over the last three years well north of $150 per person. For those wondering what the holiday might cost compared to last year during this stretch of elevated inflation, LPL Research’s Valentine’s Day Inflation Index is the answer.

Give the Gift of Time…or Jewelry

We’ve divided our Valentine’s Day Index into four components [Figure 1], capturing four favorite ways to celebrate the day. When it comes to romance the best gift is time together, and that’s where three of the four components are focused. In fact, it’s probably not bad general life advice to make spending time with the people you care about at least three times as important as material wants. Our three components for spending time together are a night in (a home-cooked meal, wine, flowers, and candy), a night out (dinner out, a sitter, and theater tickets), and a vacation getaway (airfare, lodging, and meals). If for whatever reason none of those quite fits your circumstances, it’s hard to go wrong with jewelry, which includes watches (hint hint). Of course, these can all be mixed and matched and there are budget options for each, but you’ll still need to deal with rising prices.

Inflation Hasn't Hit Valentine's Day as Hard

Thankfully, inflation hasn’t hit Valentine’s Day as hard as the broad economy. Our Valentine’s Day Index looks at annual prices, and while the index matches 2021 Consumer Price Index (CPI) inflation, at 7%, it’s lower beneath the surface. Two of three components (Night In and Night Out) are materially lower. Vacation Getaway inflation is higher, but that’s after a sharp COVID-19-related decline in 2020, so the two-year price movement is just under 1% a year. But even so, the Valentine’s Index is relatively affordable compared to inflation in the broad economy, and each component is still at a 10-year high. The relative affordability of the Valentine’s Day Index is as much about what’s not in it as what is. Energy commodities (+49% in 2021) and used cars and trucks (+37%) are both noticeably absent. Some of the other categories that saw double- digit inflation in 2021 that you can avoid on Valentine’s Day: living room, kitchen and dining room furniture (+17%), washing machines (+12%), men’s suits (+11%), and new cars (+12%). Car rental (+36%) was also very high, so if you do travel choose an option where cabs or ride services will do.

A Night in and a Night Out Remain Relatively Affordable

Looking at the cost of an evening in, while prices for candy, a home cooked meal, and flowers were all roughly in line with core CPI inflation (which excludes food and energy), the fourth element, a glass of wine at home, has seen next to no price increase at all (In case you were wondering, the Bureau of Labor Statistics does specifically track the price of wine for home consumption). However, you may want to think about what you’re cooking since some food prices have climbed quite a lot. Prices for meat, poultry, fish, and eggs were up about 12% in 2021; fruits and vegetables were up about 5%; but your best option may be to skip dinner and go right to dessert sundaes, since dairy prices were only up about 2%. Prices for a dinner out, up almost 7%, have climbed more quickly than a dinner in, but childcare costs have remained relatively restrained so it won’t cost you that much more in 2021 to hire a sitter, if you can find one. Responsible older siblings are always a good budget option, but take years of advance planning. When it comes to a vacation getaway, hotel prices have picked up dramatically in the last year, up nearly 28% after falling 11% in 2020. Airfares also collapsed dramatically in 2020, falling almost 20%, but have barely budged in 2021, climbing a little over 1%. However, airfare costs are off to a soaring start in 2022, up over 2% in January alone, likely due to rising fuel costs. Jewelry is the component that saw the largest price gain in 2020 and 2021 combined, at 4.1% annualized, but from 2012 to 2019 jewelry prices actually fell slightly, compared to gains in all other categories, so it’s probably not a bad time to potentially buy something sparkly for your sweetheart if that’s how you’re inclined.

Time is Still the Greatest Gift

We have fun with Valentine’s Day and the opportunity to treat ourselves and our loved ones with small extravagances. After almost two years of navigating COVID-19 and the impact it’s had on our lives, this year we especially relish the opportunity to stare down inflation and restrictions and celebrate with loved ones. In the big picture, Valentine’s Day is the ultimate budget holiday since time spent together is really what it’s all about. Inflation can’t touch that. Happy Valentine’s Day. Ryan Detrick, CMT, Chief Market Strategist, LPL Financial

Barry Gilbert, PhD, CFA, Asset Allocation Strategist, LPL Financial ______________________________________________________________________________________________ IMPORTANT DISCLOSURES This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy. U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio. All index data from FactSet. This research material has been prepared by LPL Financial LLC. Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity. Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-1043750-0222 | For Public Use | Tracking # 1-05243907 (Exp. 2/23)

After a tough start for stocks in 2022, investors are looking for reasons to expect a rebound. After more than doubling off the pandemic lows in March 2020, without anything more than a 5% pullback in 2021, stocks probably needed a break. That doesn’t, however, make this dip feel much more comfortable. Here we cite some reasons we don’t expect this selloff to go a lot further, though a 10% drawdown in the S&P 500 seems reasonable to expect.

Tough start to the year

It’s been a rough few weeks for the stock market. Fears of rising rates and the Federal Reserve pulling back its stimulus more aggressively than previously anticipated to fight high inflation have caused most of the market jitters, though earnings season—albeit in the very early stages—hasn’t helped either. The pain has been particularly acute for the many growth stocks that make up the Nasdaq Composite, which has corrected 14% from its November 2021 high. This is the third worst start to a year ever for the Nasdaq (down 10% year to date), though it was positive the rest of the month the last five times it was down 5% or more year to date through January 20 (thank you to our friends at Bespoke Investment Group for that nugget). Small caps have been hit even harder, with the Russell 2000 Index nearly in bear market territory with its 18% decline since November 8, 2021—though the higher quality S&P 600 small cap index has fared better in losing 12% during this period.

What might get this market turned around

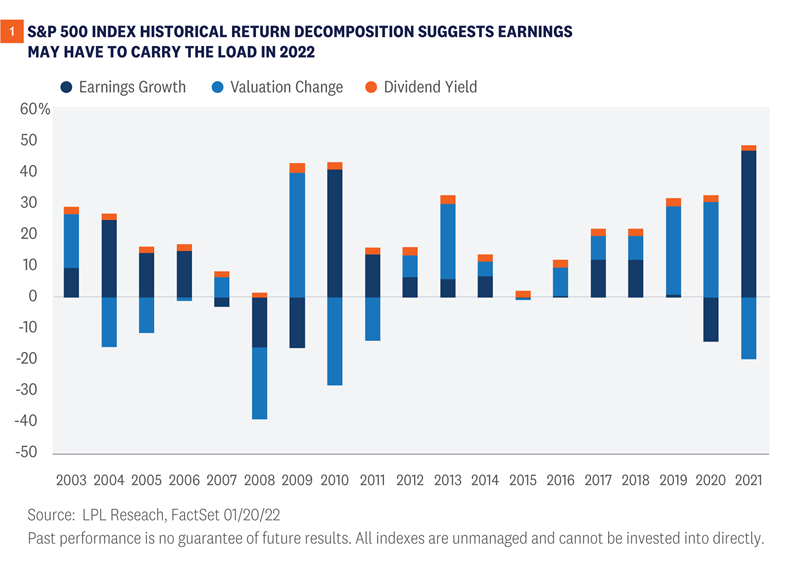

So what might turn this market around? Stabilization in interest rates would help. The 10-year Treasury yield’s inability to break through 1.9% last week and subsequent dip below 1.8% is a good start. Stock valuations are interest rate sensitive and harder to justify if bond yields go much higher (the price-to-earnings ratio for the S&P 500 using the 2022 consensus estimate for earnings per share is currently a touch below 20). On inflation, clearly a key risk for markets right now, the data likely won’t change much in January when it’s reported in February. However, we could soon see more evidence of easing supply chain bottlenecks and more people jumping into the workforce as COVID-19 disruptions hopefully fade (there are a near-record 10.5 million open jobs in the U.S. now compared to less than 7 million pre-pandemic in December of 2019). When the market begins to gain more confidence that inflation will start coming down, hopefully as winter turns to spring, inflation may turn from stock market detractor to a contributor. A Fed meeting this week without any negative surprises would also help. Stable or lower oil prices would help as well. What about earnings as a potential catalyst? As we suggested in our 2022 Outlook: Passing the Baton, earnings growth would likely be the primary source of stock market gains this year. The downward pressure on stock valuations from higher interest rates makes that more likely. In Figure 1 we have decomposed annual returns for the S&P 500 into earnings growth, valuation changes, and dividend yield. During 2019 and 2020, when the S&P 500 returned 24.7% annualized (55.7% cumulative), increases in valuations drove much of the gains. That changed last year when earnings rose an estimated 50% and valuations contracted. We expect 2022 to look more like the mid-cycle mid-2000s or mid-2010s with more modest returns, more contributions from earnings growth and dividends, and little, if any, contribution from valuation. That begs the question whether corporate America has enough earnings power still left in the tank to get investors excited about buying this latest dip. We wrote about the challenges facing corporate America this earnings season in our earnings preview, including supply chain disruptions, wage and other cost pressures, and the Omicron COVID-19 variant, all of which make it tough to predict if earnings season will be a catalyst for a turnaround. Still, we lean toward the rest of earnings season providing some support for stocks for these reasons:

Despite these challenges, with about 70 S&P 500 constituents having reported, index earnings are still tracking to 5% upside, in line with the long-term historical average.

Profit margin assumptions baked into analysts’ estimates appear to reflect these challenges, increasing the likelihood of mostly positive market reactions to results.

Despite a likely smaller upside surprise than in recent quarters, an earnings growth rate potentially in the mid-to-high 20s for the quarter is still impressive.

Estimates for 2022 have been holding up well. Historically, earnings estimates fall during reporting season, which isn’t happening so far.

Volatility is uncomfortable but normal

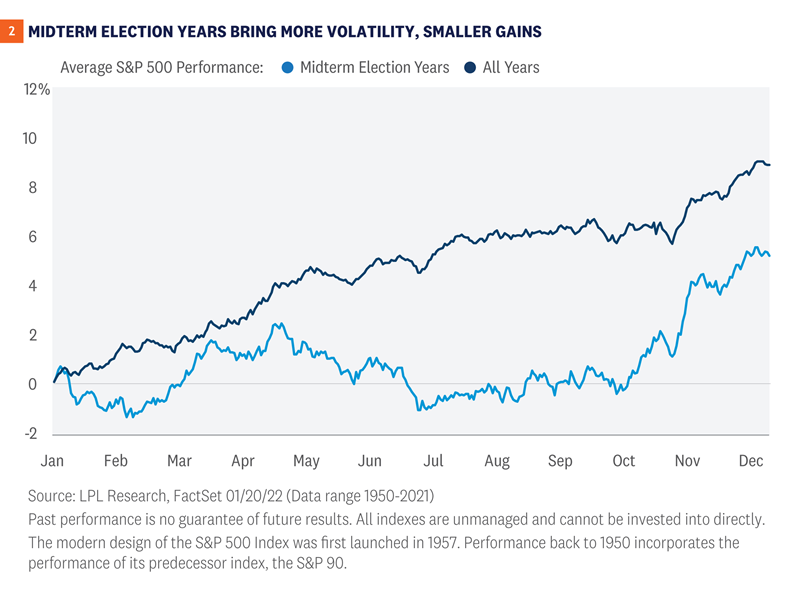

Investors have grown accustomed to steady, consistent gains over the past couple of years which makes the current bumpy ride feel more uncomfortable. After no more than a 5% pullback in 2021 and the S&P 500 having more than doubled off the March 2020 lows, we have been anticipating more volatility in 2022. Higher interest rates and less accommodating monetary policy from the Fed amid stubbornly high inflation are getting most of the blame, and probably deservedly so. But another reason for the rough start to the year could be policy driven. It is a midterm election year, which typically brings more volatility and smaller gains. As shown in Figure 2, historically during mid-term years the S&P 500 has on average done nothing but bounce around the flat line until right before midterm elections, much different than the average path of the market across all years. Although we would argue these midterms may bring less uncertainty than some others in recent decades given gridlock appears more likely than not to most political strategists, policy uncertainty is still there and the environment remains divisive. As a result, we would not be surprised if this year ended up looking more like the typical midterm year with mid-single-digit gains for stocks rather than double-digit gains, and a better second half than first half. It will take time for the biggest clouds to clear (COVID-19 and inflation) and stocks have historically seen very strong rallies after midterm elections pass.

Conclusion

This volatility we’ve seen this year is uncomfortable, but it is well within the range of normal based on history. The S&P 500 has averaged three pullbacks of 5% or more per year and one correction of at least 10% per year over its long history. After just one 5% dip last year, and huge gains off the 2020 lows, we were due for a dip. This pullback in the S&P 500 could easily go to 10%, or even a little more. The average max drawdown in a positive year for stocks is 11%. But based on the still solid overall economic and earnings backdrop, our expectation that the inflation clouds may soon start to clear, and the stock market’s historically solid track record early in Fed rate hike cycles, we wouldn’t expect this pullback to go much further. We continue to see fair value on the S&P 500 at year end at 5,000-5,100, more than 12% above Friday’s closing price at the low end. Jeffrey Buchbinder, CFA, Equity Strategist, LPL Financial

Ryan Detrick, CMT, Chief Market Strategist, LPL Financial

______________________________________________________________________________________________ IMPORTANT DISCLOSURES This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy. U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio. All index data from FactSet. This research material has been prepared by LPL Financial LLC. Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity. Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-1013950-0122 | For Public Use | Tracking # 1-05235161 (Exp. 1/23)

In many ways, 2021 was a typical year for markets, but it also reinforced some basic market lessons that are hard to learn, even if they are not new. As we launch into the New Year, we’re highlighting three 2021 market lessons that we think may matter for 2022: 1) equity valuations are a poor timing mechanism, 2) structural forces have a large influence on interest rates and may keep them relatively low, and 3) politics and markets don’t mix. Welcome to the New Year for markets, when year-to-date returns all reset to 0% and the year ahead is still a blank slate. No doubt, 2022 will provide its usual mix of ordinary market behavior and unexpected surprises. While these surprises can’t be forecasted, we can say with near certainty that we’ll have some. At the same time, markets have patterns that tend to repeat, even if the emphasis is different from year to year. As we head into the New Year, we’re taking a look back at 2021 and drawing out three lessons that we think will matter for 2022.

Valuations Aren't a Short-Term Market Timing Mechanism

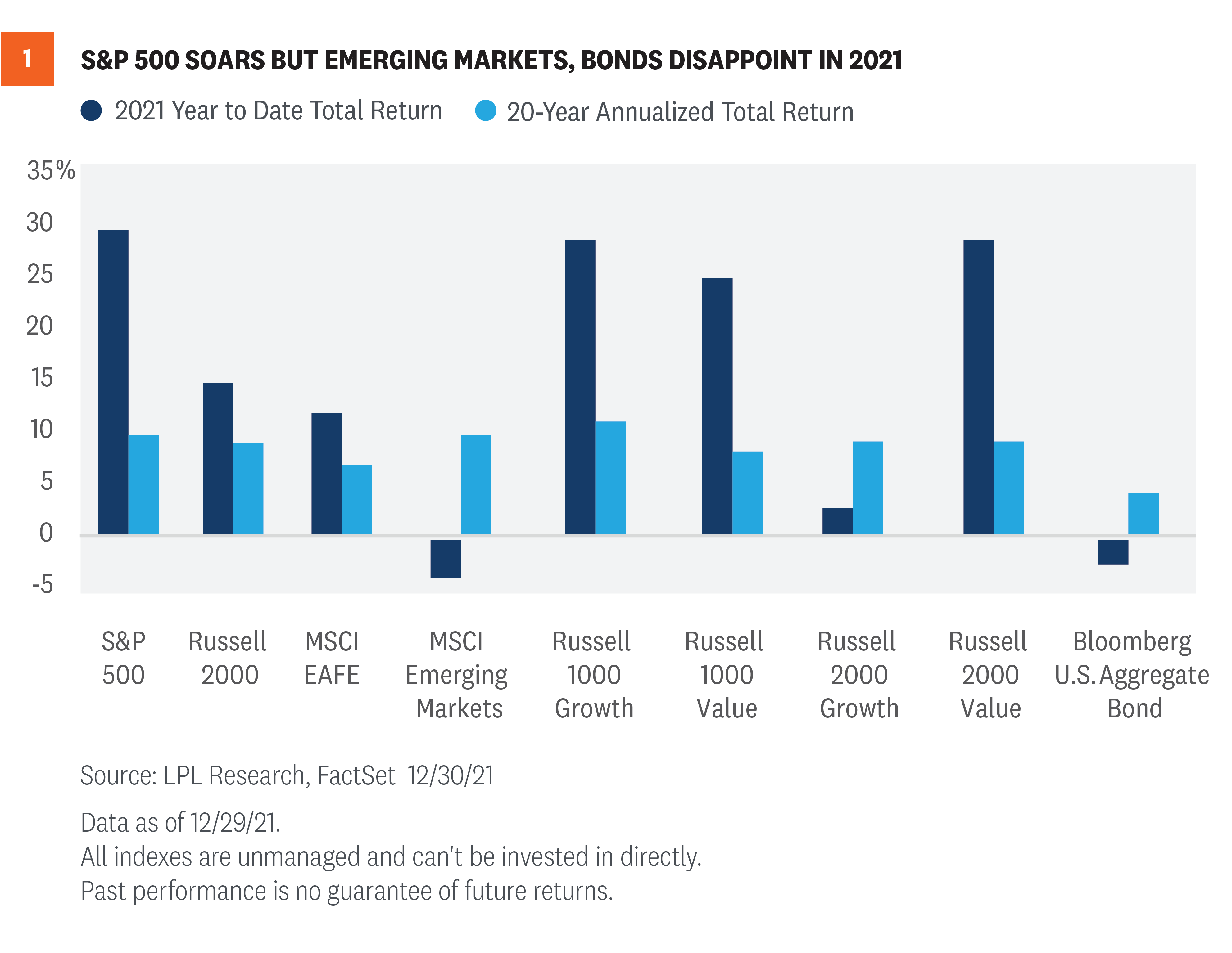

At the start of 2021 we heard concerns that broad U.S. markets were overvalued using many traditional valuation metrics, such as the price-to-earnings ratio (PE). In addition, compared to the U.S., international stocks (both developed and emerging markets) looked relatively cheap. But as shown in Figure 1, the S&P 500 surged higher in 2021, performing well above its historical average, while international equities lagged behind the U.S., with weakness in emerging markets in particular. Once again, valuations were a weak short-term timing mechanism. At the start of 2021, the PE for the S&P 500 was historically elevated at almost 22.5 on forward earnings according to FactSet data. At the same time, interest rates were extraordinarily low, which makes stocks attractive relative to bonds and increases the present value of future earnings. On top of that, an extraordinarily strong year for corporate earnings helped stocks “grow into” their valuations, with the PE actually falling to nearly 21 by the end of the year despite strong stock market gains. Sentiment is often the primary culprit for allowing valuations to remain elevated, and it did play a role in 2021, but market fundamentals were even more important. If investors favored stocks in 2021, it was more about a sizable upside surprise in earnings growth than elevated optimism. The underperformance by international equities this year, which may have surprised some, also reminds us that valuations are not a timing tool. International stocks have been more attractively valued than U.S. stocks for quite some time and yet, they’ve underperformed consistently for over a decade. We believe valuations should be used in combination with technical analysis, which helps measure both sentiment and captures collective market wisdom, to help inform investment decisions. Signals from the charts have helped us side-step some of that performance drag. Also, keep in mind that Europe and Japan are more value-oriented markets than the U.S., so growth-style leadership here at home makes it very difficult for these international markets to keep up. We continue to favor the U.S. over developed international markets for 2022 because of the relatively healthier U.S. economic growth outlook and strong U.S. dollar, but international equities may become increasingly attractive as COVID-19 restrictions are removed globally.

Structural Forces Continue to Weigh on Interest Rates

If someone had told you at the start of 2021 that inflation (as measured by the Consumer Price Index) would be up close to 7% over the year while real gross domestic product (GDP) would grow near 5.5% and asked you where the 10-year Treasury yield would be at the end of the year, most market experts would likely guess well above the approximately 1.50% where we ended the year. It’s true 2021, by many accounts, wasn’t a very good year for core fixed income investors—although that was largely to be expected. Coming into the year, interest rates were still amongst the lowest they have ever been and we thought they were headed higher—and they did. As such, returns for core fixed income investors, as measured by the Bloomberg U.S. Aggregate Bond Index, were negative for the year for only the fourth time in the index’s history dating back to 1976. However, after a 70 basis point (0.70%) increase in the 10-year Treasury yield by mid-March, which led to one of the worst starts to the year ever for core bonds, yields have largely remained range bound. One of the main reasons interest rates have stayed as low as they have this year was the amount of foreign interest in our markets. Despite relatively low yields in the U.S., many foreign investors are still better off investing in U.S. fixed income markets. With approximately $13 trillion in negative yielding debt globally (it’s still crazy to think that you have to pay a country/company to own its debt), even modestly positive yielding debt is an attractive option. This has certainly helped keep interest rates from moving significantly higher—a likely headwind to higher rates in 2022 as well. So what is the key takeaway from 2021? Despite increased inflationary pressures not seen since the 1980s (when 10-year Treasury yields averaged over 10% for the decade), there is still a huge global demand for safety, income, and liquidity in portfolios and that has kept interest rates (and spreads) from moving much higher. While yields for U.S. core fixed income may seem low, the role it plays in portfolios is still an important one.

Politics and Investing Don't Mix

This is one lesson we likely knew before the year began, but 2021 provided another strong example of why politics and investing don’t mix, both for broad markets and for the market impact of more specific policy. For example, when President Biden was elected, one of the sectors most expected to suffer was traditional energy. The bear case for energy was that Democratic policies towards fracking and the fossil fuels industry would further harm one of the worst performing sectors over the past decade. In contrast, the solar industry was expected to benefit from an acceleration towards renewable and clean energy sources. Well, what happened? The complete opposite. The S&P 500 Energy Sector was by far the top performing sector of the year, up more than 50%, while the MAC Global Solar Energy Index, a basket of stocks focused on solar energy, fell nearly 30%. And this isn’t the only time in recent history we have seen the energy sector returns upend traditional thinking. When President Trump was elected back in 2016, the two consensus sector winners from his presidency were expected to be energy and financials due to deregulation. However, from the date of the 2016 Presidential election to the 2020 election, energy stocks were cut in half while the financials sector returned less than half that of the broader market. Forecasters had the policy right and the business impact was generally as expected, but nevertheless it seemed small from a pure market perspective compared to other drivers influencing sector returns. Speaking more broadly, stocks have done extremely well over the past decade, with little regard or correlation to which party has held the White House or Congress, and we believe investors would do well to remember that in 2022 as midterm elections begin to dominate the news cycle. It’s not that policy prognostications are incorrect or that policy doesn’t matter. Rather, when it comes to markets there are larger economic forces in play that typically matter a lot more.

What Lies Ahead in 2022

We do not expect 2022 to simply be a repeat of 2021. We’ve moved further toward the middle of the economic cycle, inflation is likely to decrease rather than increase, and economic momentum will probably slow. But perhaps most importantly, the policy support from central banks and governments that have helped global economies bridge the economic fissures left by COVID-19 will likely begin to fade, leaving the economy to stand increasingly on its own two feet while putting more emphasis on the aggregate decisions of businesses and households. (For a broad overview of our expectations for 2022, see our Outlook 2022: Passing the Baton.) But for all the differences, we expect some important lessons learned in 2021 to matter in 2022, and as the year evolves we’ll continue to monitor and share the market signals that will help shape the market environment in the New Year. Barry Gilbert, PhD, CFA, Asset Allocation Strategist, LPL Financial

Ryan Detrick, CMT, Chief Market Strategist, LPL Financial

Jeffrey Buchbinder, CFA, Equity Strategist, LPL Financial

Lawrence Gillum, CFA, Fixed Income Strategist, LPL Financial ______________________________________________________________________________________________ IMPORTANT DISCLOSURES This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy. U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio. All index data from FactSet. This research material has been prepared by LPL Financial LLC. Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity. Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-994650-1221| For Public Use | Tracking # 1-05227512 (Exp. 1/23)

The near-10% correction in the S&P 500 Index and even larger drawdown in the Nasdaq have gotten a lot of attention this year. What hasn’t gotten as much attention—and maybe surprising to some—is the relative resilience in equity markets outside the U.S. In our special Winter Olympics edition of the Weekly Market Commentary, we hand out medals to the U.S., developed international, and emerging markets. Who do we think will get the gold? Read on to find out.

U.S. Has Been Skiing Uphill

It’s been a rough start to the year for U.S. stocks with some stiff headwinds. The path of the S&P 500 in January looked like something Mikaela Shiffrin might ski on given the steepness of the decline with twists and turns. Fears that the Federal Reserve (Fed) might be behind the curve in its inflation battle got most of the blame for the market selloff, while a few high-profile earnings misses—Meta (Facebook) being the latest—have added to investors’ anxiety levels. Meanwhile, the international equity markets have held up relatively well. The S&P 500 Index is down 5.6% year to date, outrun by the 3.8% and 0.9% declines in the MSCI EAFE Index (developed international equities) and the MSCI Emerging Markets (EM) Index. To assess which regional market might come out on top at the end of the 2022 competition, we take a look at global fundamentals, valuations, and technicals.

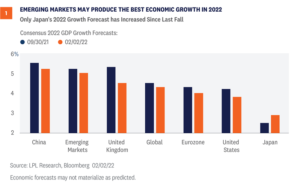

Economic Growth Likely to be a Close Race

Starting with economic growth outlooks, emerging markets may produce the fastest gross domestic product (GDP) growth in 2022, but it could be a close finish [Figure 1]. China’s zero-COVID-19 policy may delay the restoration of the EM growth premium while we wait for an eventual end to the pandemic. Meanwhile, distressed property developers present a headwind to growth, though monetary stimulus is helping turn the tide some in China in the near term. We expect developed international and U.S. economies to generate similar growth in 2022, though rising forecasts for Japan are encouraging. Europe may also see more benefit from pandemic-related pent-up demand as the region is earlier in its economic cycle than the U.S. And U.S. growth has gotten off to a slow start in the first quarter because of the Omicron variant.

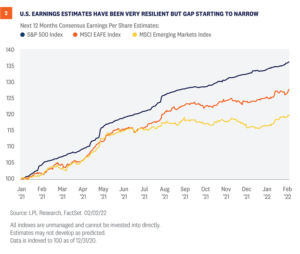

U.S. the Clear Favorite in the Earnings Event

The U.S. comes into 2022 as the earnings favorite. Consensus estimates are calling for a 9% increase in S&P 500 earnings this year, ahead of the 5% and 7% increases expected for developed international markets and EM, respectively. As shown in Figure 2, U.S. earnings estimates have marched steadily higher over the past year, outpacing the increases outside of the U.S. While it’s tempting to think EM will generate better earnings growth because economic growth is better, EM companies have had a difficult time translating economic growth into profits over the past decade (certainly part of the reason why valuations are low in EM, as discussed below). In addition, China’s regulatory crackdown still presents earnings risk even though the headlines have settled down. On the flip side, the recent increase in EM earnings estimates for 2022 is encouraging (2.7% over the past month, compared to 1.5% for the U.S. and 2.3% for developed international). So while we consider EM an earnings underdog in 2022 and consider it more of a show-me story, it’s only a small hit to its medal hopes.

U.S. Skating on Thin Ice When it Comes to Valuations

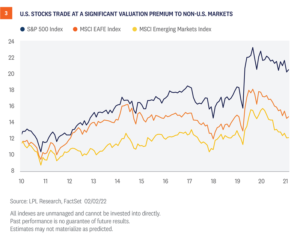

The valuation competition is the clearest cut. Figure 3 shows that U.S. stocks continue to trade at a significant premium to their international and EM counterparts and have for a long time. In fact, developed international stocks, measured by the MSCI EAFE Index, are trading at a 28% discount to the S&P 500 on a forward price-to-earnings (PE) basis. That discount is the largest in at least 30 years, and probably much more if we had data going back farther. Emerging market stock valuations are not in uncharted territory like developed international, but at a 40% discount to the S&P 500’s forward PE, a 20-year low, EM is clearly attractively valued. If we knew the earnings would come through this year, EM would warrant consideration for the gold medal in the valuation competition, but we’ll give it to developed international given the unprecedented discount and greater earnings predictability.

Technicals Still Favor the U.S., For Now

When we compare the charts of developed international and emerging markets to the U.S., the trend still favors a home-country bias. Relative to the S&P 500, both the MSCI EAFE and MSCI EM indexes remain below downward sloping 200-day moving averages, a simple but effective measure of a downtrend. That said, we’re open to the idea of that trend changing at some point in 2022. Both regions have outperformed the U.S. year to date, but for unique reasons. Developed international markets such as Europe and Japan, which are more value-oriented markets, have benefited from having fewer high-flying tech stocks, while some segments of the Chinese technology sector have finally begun to show signs of stabilization after falling more than 50% last year. One potential tailwind that could benefit international equities this year is the U.S. dollar. After surprising many investors and rising throughout 2021, the U.S. dollar began to show signs of topping in December. Last week the U.S. Dollar Index suffered its worst week since 2020, and a continued reversal lower should benefit holders of international equities.

Conclusion