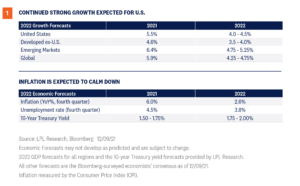

We believe pent-up demand, gradual improvement in supply chain challenges, solid labor force growth, and productivity gains will all contribute to another year of above-trend economic growth in 2022. COVID-19-related risks remain and the potential for a policy mistake may be elevated as the economy moves towards normalization, but we think the overall environment will be supportive of business growth and ultimately equity markets The U.S. economy bounced back from its worst year since the Great Depression in 2020 with one of the best years of growth in nearly 40 years in 2021. A combination of record stimulus, a healthy consumer, an accommodative Federal Reserve (Fed), vaccinations, and reopening of businesses all contributed to the big year. In what amounted to the shortest recession on record, only two months in March and April 2020, the economy came roaring back to produce what is currently expected to be over 5% GDP growth in 2021, more than making up for the 3.4% drop in GDP in 2020. Of course, there have been hiccups along the way. You can’t shut down a $20 trillion economy and then expect it to get going again without warming up first. Supply chain backlogs, materials and labor shortages, and higher prices all held the economy back to varying degrees. The good news is, demand is still very strong, and as the backlogs unwind (which could take years in some cases), we expect above-trend economic growth and see low risk of a recession in 2022. As the U.S. economy moves more to mid-cycle, our 2022 forecast is for 4.0–4.5% GDP growth in 2022 [Figure 1]. While a slowdown from 2021, it’s still a very solid number. We expect inflation to tame from 2021 levels to a potential run rate under 3% by the fourth quarter with core inflation numbers lower, a step in the right direction, although it may still be on an upward trajectory the early part of the year. Globally, Europe and Japan were hit especially hard by the pandemic in 2021. But as COVID-19 cases potentially fall globally, those areas could be ripe for better economic growth in 2022. Meanwhile, emerging market economies may disappoint as growth in China could be constrained by regulatory crackdowns.

TIME FOR A HANDOFF

Fiscal and monetary policy played big roles in the economic recovery in 2021, but we see 2022 playing out as a handoff—from stimulus bridging a pandemic recovery to an economy growing firmly on its own, with consumer demand, workforce gains, productivity, small businesses expansion, and capital investment all playing parts in the next stage of economic growth. You have to give the U.S. consumer credit for continuing to drive the economy forward, and 2022 shouldn’t change that. Don’t forget, it took retail sales only five months to get back to pre-COVID-19 levels after the lockdowns in March and April 2020. Bottlenecks and the Delta variant surge have done little to slow an eager consumer. With likely still low interest rates, increased equity in people’s homes, nearly $3 trillion in money markets (retail and institutional), and another $3.5 trillion in excess liquidity in bank accounts, the consumer should remain quite healthy in 2022. Like every other time in history, those who adapt will survive. Businesses have already started to adapt to the new world, which may help productivity increase in 2022, as output-per-hour (productivity) potentially starts to accelerate again. Productivity allows for stronger growth and can help contain inflation, since more goods and services are produced. The 1970s was known as a time of high inflation, but it was also a time of very low productivity—fortunately a scenario we don’t see happening this time around. Another key to the economic transition may be capital expenditures (capex). These include business investment in property, plants, buildings, technology, and equipment. These investments could boost overall productivity and overall output, but might take time to build, so the results could be years away in some cases. Additional capex spending would be one of the best ways to see if corporate America is indeed over the shock of the pandemic and ready to invest for future growth opportunities. Standard and Poor’s data shows capital expenditures are expected to have grown an impressive 13% in 2021 and likely even more in 2022. In fact, the capex rebound in this recovery has already been faster than previous downturns, with plenty of room to go in our view. And it isn’t just a U.S. theme, as 2021 was likely the best year for European capex since 2006, and the global chip shortage has led to major investments in Japan and South Korea as well.

THE EVERYTHING SHORTAGE

2021 was the year nearly everything was in a shortage, and it all translated to added inflationary pressure. Record numbers of ships waiting at ports, a lack of materials, unfilled job openings, higher commodity prices, a lack of truck drivers, major backlogs, and supply chain disruptions all added to the larger price increases seen essentially across the board in 2021. While we do believe these pressures will steadily decrease over the next year and inflation will eventually settle back to 2–2.5%, it will likely be a gradual process. While inflation is broadly elevated, some key core elements remain more stable, and we believe these will be the center of gravity over time for some of the more volatile price changes we’ve seen. Still, supply chains may take a year or two to be fully addressed, depending on the product and the scale of the problem. Despite challenges around supply chains, hiring, and prices, if the demand is there it should help drive continued improvement as businesses adapt to address challenges. That is likely to leave us with a positive economic backdrop for at least 2022, and maybe much longer, despite current inflation levels.

HOW MUCH TIME LEFT?

Let’s face it, this wasn’t your average recession. Some industries actually did better during the pandemic, while segments of other industries were severely constrained. Spending patterns shifted. Stimulus was delivered quickly on a massive scale. How strange did that make it? This was the first recession in history that saw FICO scores go up. Recessions are necessary to wash out the excesses, but some imbalances weren’t worked off this time around. For this reason, we think this economic expansion could be mid-cycle much sooner and likely won’t be as long as the record 10 years we saw last cycle. The average expansion since World War II has been just over five years, suggesting there are still potentially several years of growth remaining, especially since we don’t see typical recessionary warning signals right now. Far from it, we anticipate above-trend growth in 2022. But we’ll be on watch early.

RISKS AND MARKET IMPLICATIONS

Our baseline economic outlook would likely provide a positive backdrop for equity markets, supporting further earnings gains while productivity gains potentially help offset some of the margin pressure from wage growth. At the same time, there are clear risks to our view. Handoffs can be fumbled and with inflation running hot and risks around COVID-19 still in play, the potential for a policy mistake is elevated. And while we’ve made substantial progress against COVID-19, ranging from vaccines to treatments to public health policy, we don’t yet have full clarity on how it will continue to impact the economy. Nevertheless, our baseline is a continued move toward normalcy as the choices of businesses and households play a bigger role in determining the shape of the expansion. Ryan Detrick, CMT, Chief Market Strategist, LPL Financial

Barry Gilbert, PhD, CFA, Asset Allocation Strategist, LPL Financial ______________________________________________________________________________________________ IMPORTANT DISCLOSURES This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy. U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio. All index data from FactSet. This research material has been prepared by LPL Financial LLC. Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity. Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-977801-1221| For Public Use | Tracking # 1-05221199 (Exp. 12/22)

After an upside inflation surprise in October, it’s clear that peak inflation may still be ahead, possibly even pushing into 2022. While the Federal Reserve (Fed) maintains its position that elevated inflation will be transitory, we have yet to see progress. Below we look at five signs to watch for over the next several months that may signal that inflation may be near or at its peak. The October reading for the Consumer Price Index (CPI), the most widely known measure of inflation, came with an upside surprise versus expectations on top of already elevated inflation concerns. The headline number came in at 0.9% for the month and 6.2% for the year, the highest reading since November 1990. The core reading (which excludes food and energy prices) rose 0.6% for the month and 4.6% for the year—the highest since August 1991. Elevated inflation continues to be largely driven by pandemic-related dynamics—primarily supply chain challenges and tight labor markets combined with high demand as the global economy bounces back. The COVID-19 Delta variant has deepened those problems in unexpected ways, although we cautioned in the early days of the surge that further supply chain disruptions were likely. Calling inflation “transitory” has not really captured these inflation dynamics well. Elevated inflation will last as long as supply chain bottlenecks and hiring challenges remain in place. As those dynamics subside, we expect inflation to return to something close to 2%, but we believe that’s more of a 2023 conversation. But market participants don’t need to wait until CPI is back under 3% to feel a sense of relief. It would be enough to know that we’re past the peak, something that might not happen until 2022. In fact, since markets are forward looking, it may be enough to have a “peek at the peak.” Here are five signs to watch for that peak inflation, if not immediately at hand, may be in the near future.

Supply Chains

Current inflationary pressure is primarily about supply chain disruptions, the inability to get product to market (whether because of labor and material shortages), the inability to maintain needed inventory, or logistical disruptions. Supply chains will heal over time—businesses have a strong profit incentive to address supply chain challenges. But there are structural constraints on how quickly progress takes place that businesses can’t control. To take one high profile anecdotal example of supply chain disruptions and the impact of structural problems, there are currently over 100 container ships waiting to unload off the ports of Los Angeles and Long Beach, California. Before the pandemic, the worst backup was under 20. But the needed equipment, space, workers to accelerate progress simply isn’t available on demand. Our best peek at how supply chains are doing may be purchasing managers’ index (PMI) readings. Supply-chain related readings from the Institute for Supply Management’s October release has shown some improvement in places, but disruptions remain elevated. The reading on order backlogs peaked in May, but at 63.6 remains well above its long-term median of just above 50 (above 50 indicates higher backlogs from the previous month). Likewise, supplier deliveries also peaked in May but has moved higher the last two months and was at a very elevated 75.6 in October. Readings in the mid to low 50s for both of these sub-indexes would probably be needed to indicate we were on the cusp of significant improvement to supply chain problems.

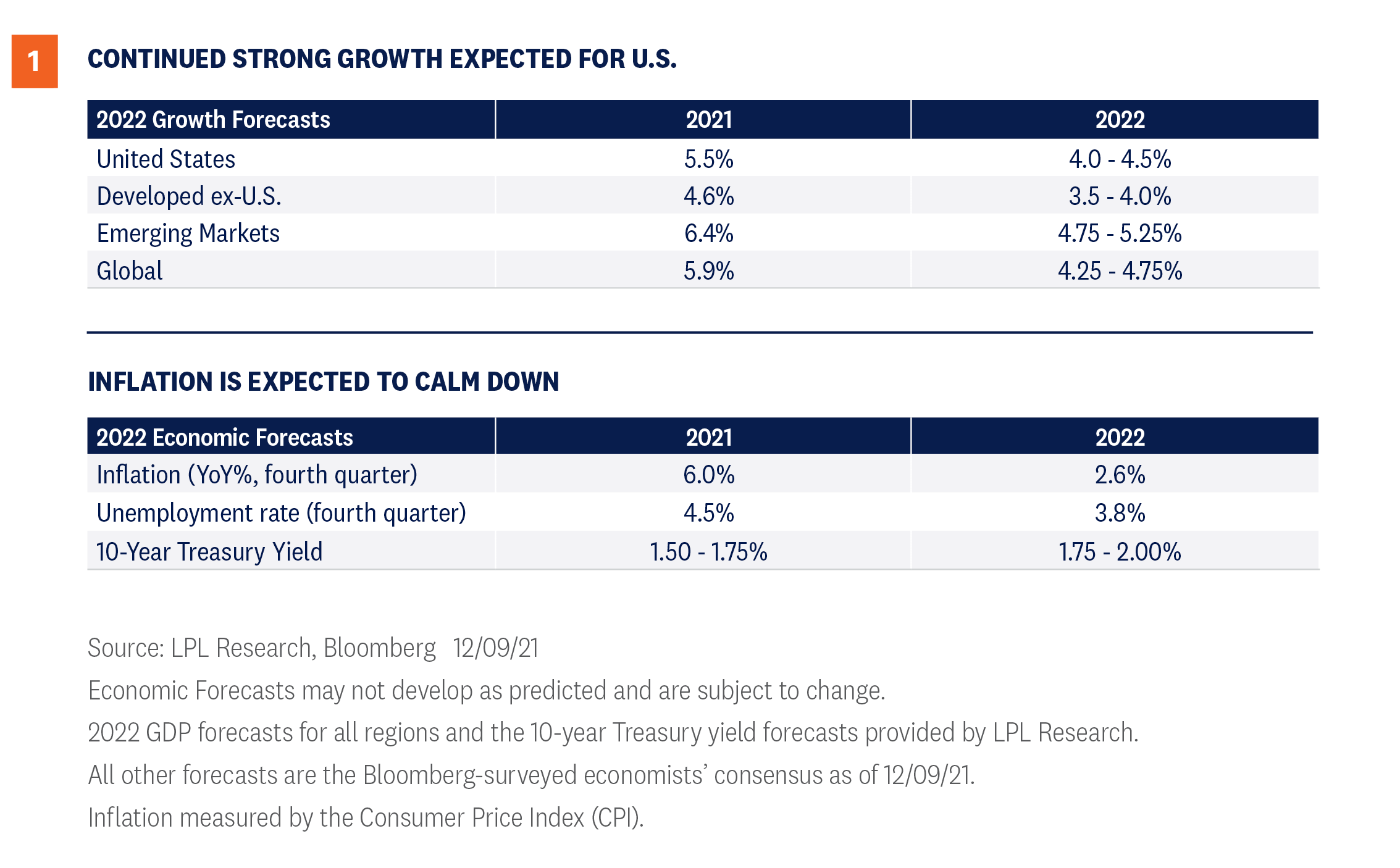

Housing and Rents

Shelter excluding energy costs, essentially housing costs and rents, makes up about 1/3 of CPI and just over 40% of core CPI (excluding food and energy). Costs for housing have picked up on a year-over-year basis but, unlike some other measures of inflation, it has not yet hit a high dating back to the 1990s [Figure 1]. In fact, current one-year housing inflation, at 3.5%, is lower than its 2019 peak. Nevertheless, housing costs have jumped the last three months and housing inflation is a concern—both because it represents such a high proportion of consumer spending and because it tends to be relatively sticky. Base effects (rolling low numbers off the one-year reading) will likely help push annual shelter inflation higher until April 2022, so looking at monthly numbers will be important. Consecutive monthly readings near 0.3% would be a good sign that housing costs have stabilized but, even at that level, the year-over-year number could continue to climb in the first several months of 2022.

Market Implied Inflation

Breakeven inflation rates, the difference between nominal Treasury yields (the number we usually hear about) and the yield for Treasury Inflation-Protected Securities (TIPS), can provide important information about inflation expectations. The breakeven inflation rate is the forward-looking reading of inflation at which TIPS would outperform similar maturity nominal Treasuries if inflation were to run higher. Because investors are willing to pay extra for a hedge against inflation, the breakeven rate tends to run higher than what true expectations may actually be. The two-year breakeven began to climb in early October 2021 after holding roughly steady since early February, and currently sits around 3.3%. The Bloomberg-surveyed economists’ consensus for average inflation in 2022-2023 is 2.8%. Since higher near-term inflation expectations will roll off as we approach peak, a return of the two-year breakeven to around 2.75% would probably indicate we have passed the peak and a decline to below 3% could be an early signal the peak is coming.

Energy and Commodity Prices

Even though energy prices are volatile compared to overall price levels, for most people prices at the pump shape their perception of inflation more than anything else. Oil prices (West Texas Intermediate) have been climbing since October 2020 and now sit above $80 per barrel compared to a level that generally hovered closer to $60 for much of 2019. Global copper prices started climbing even earlier, beginning their advance in May 2020. Both oil and copper prices can stay elevated for some time and it’s not as easy to target a particular signal that inflation may be settling down. Copper has already shown some stabilization since peaking in May and while base effects will be in play until April 2022, stability around current levels until the end of the year (or any sharp decline) would be a good signal inflation may soon peak. The picture on oil isn’t as clear. Oil maintained a range above current levels from 2011 to 2014, but CPI was still running under 2% for much of that period. If oil were to hover near $80 barrel into early 2022 with no significant advance, it would be a positive sign that inflation may be peaking, but we wouldn’t take it as a negative sign if it pressed higher.

Consumer Sentiment

Influenced by prices at the pump, consumer inflation expectations have skyrocketed. While not the best predictor of inflation, inflation expectations can have an effect on actual inflation and is monitored by the Fed. The Conference Board’s survey of consumer inflation expectations twelve months from now climbed to 7% in October. The New York Federal Reserve Bank’s consumer survey has also seen expectations spike, but to a more moderate (but still very elevated) 5.65% in October. Both of these numbers are well outside of norms. For consumer expectations, just seeing the numbers begin to settle down would be enough to signal we were potentially near the peak. The Conference Board’s survey has a longer history, and typically spikes in expectations have been short lived. Current expectations have been over 6% for the last 11 months, with the most recent reading the highest. Expectations moving back below 6% would be an important signal we may be near or at the peak.

Conclusion

For market participants, the main inflation takeaway is how it might influence the Fed’s timeline for starting rate hikes. When evaluating that, we believe it’s important to factor in the Fed’s understanding of how a rate hike would impact the kind of inflation we’re dealing with. A rate hike usually helps to control inflation by slowing demand when an economy is overheating. But it can’t help ships unload containers more quickly or help address order backlogs. We still see the first rate hike likely coming in early 2023, especially if there are strong signals inflation has peaked. But if rising housing costs and consumer expectations make higher inflation stickier, we could see the first rate hike pulled into 2022. Whichever way it goes, you’ll know some of the key signals to watch for. Barry Gilbert, PhD, CFA, Asset Allocation Strategist, LPL Financial

George Henry Smith, CFA, CAIA, CIPM Senior Analyst, LPL Financial ______________________________________________________________________________________________ IMPORTANT DISCLOSURES This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy. U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio. All index data from FactSet. Please read the full Outlook 2021: Powering Forward publication for additional description and disclosure. This research material has been prepared by LPL Financial LLC. Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity. Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-892982-0921 | For Public Use | Tracking # 1-05212142 (Exp. 11/22)

The S&P 500 Index has gained more than 20% so far this year, making more than 50 record highs along the way. Certainly nobody should be upset with that return if that was all 2021 brought us. However, we see signs that there could be more gains to come in the final two months of the year. Seasonal tailwinds, improving market internals, and clear signs of a peak in the Delta variant all provide potential fuel for equities heading into year-end, and we maintain our overweight equities recommendation as a result.

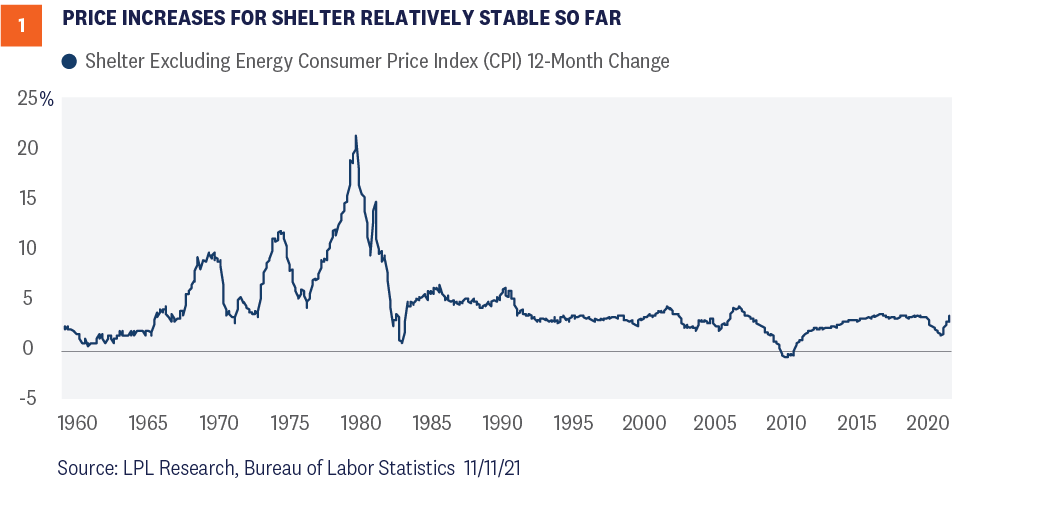

Late October is the Seasonal Low

One of the most important points we believe investors should recognize is that there has been a sort of stealth correction going on throughout most of the summer, consistent with the historically weak period commonly referred to as “Sell in May and Go Away.” While the S&P 500 has returned more than 8% since the end of April, the average individual stock in the index suffered more than a 10% correction. Meanwhile, the average stock in the Russell 2000 Index (covering small cap equities), which is almost unchanged over that period, suffered a more than 25% bear market. However, as shown in [Figure 1], late October has historically marked the seasonal low before stocks typically rally into year-end. In fact, the fourth quarter as a whole is by far the strongest quarter historically, on average, with the S&P 500 rising 4% and finishing higher nearly 80% of the time. November, meanwhile, is the strongest month of the year—both since 1950 and over the past decade. So, whether you believe that stocks have thus far followed the historical pattern of summer weakness that should be ending, or that the current price trend is so strong that it was able to buck the summer doldrums, we see ample reason to believe that seasonality has now turned from a headwind for equities to a tailwind.

Improving Market Internals

Seasonality is something that we want to be aware of, but perhaps more important to our thesis is what technicals and market internals are showing us right now. As we just discussed, much of the market has corrected over recent months, but are key groups showing signs of improvement? The answer is clearly yes. Economically sensitive groups of stocks, commodities, and even bond yields had largely stagnated since early May—but have recently reaccelerated. For example:

The S&P 500 Financials Sector just broke out to a new all-time high after being largely unchanged from May 7 through October 13.

The Dow Jones Transportation Average is up more than 10% in October alone—and at a three-month high after suffering a 13% correction.

Copper, often referred to as Dr. Copper for its ability to forecast economic conditions, has gained more than 10% since bottoming in August.

The yield on the 10-year U.S. Treasury is up more than 50 basis points (0.50%) since its low in July.

Consumer discretionary stocks have outperformed consumer staples stocks by 10 percentage points in the past two months after lagging them for much of the summer.

There are certainly more examples, but let’s not forget perhaps the most important indicator: price. After finally suffering its first 5% pullback of 2021 in early October, the S&P 500 has come roaring back and closed at a record high on October 21. We firmly believe that new highs are something to be embraced, not feared, and history shows that new highs tend to come in bunches—something that has certainly been true so far this year.

Data Strong Amid Clear Signs of a Delta Peak

Though the above points may be construed as a technical argument for strength into year-end, make no mistake: The fundamentals are improving in real time as well. The rolling seven-day rate of new COVID-19 cases has fallen over 60% from its peak in early September. No doubt connected to the decrease in cases, jobless claims have fallen steadily in recent weeks, with continuing claims sliding below 2.5 million for the first time since the pandemic began. Recent economic data shows that Americans have taken notice of the improved outlook. Economists expected retail sales to fall slightly in September, but the report showed that overall retail sales grew 0.7%. Despite the impact of the COVID-19 Delta variant wave, retail sales have grown three of the past four months, providing further evidence of the strength of the U.S. consumer. Finally, the U.S. Bureau of Labor Statistics (BLS) latest Job Openings and Labor Turnover Survey (JOLTS) report showed that the number of American workers who are voluntarily quitting their jobs is at its highest rate since the BLS started publishing data in 2001. Typically, quits are viewed as a sign of a strong economy and healthy labor market, as the most common reason for people voluntarily leaving their job is to start a new one—something workers are more hesitant to do in times of economic uncertainty.

Conclusion

LPL Research continues to believe that tactical investors should tilt portfolios in favor of stocks over bonds relative to their respective targets. Modestly rising interest rates and tight credit spreads reflect a healthy and improving economy, but should add pressure to fixed income returns in the near-term. Meanwhile, a bullish part of the calendar, improving equity market internals, and falling COVID-19 cases may clear the way for a potentially bullish environment for equities through year-end. Ryan Detrick, CMT, Chief Market Strategist, LPL Financial

Scott Brown, CMT, Senior Analyst, LPL Financial ______________________________________________________________________________________________ IMPORTANT DISCLOSURES This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy. U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio. All index data from FactSet. This research material has been prepared by LPL Financial LLC. Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity. Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-934700-1021 | For Public Use | Tracking # 1-05204667 (Exp. 10/22)

Get a head start on your financial future with LPL Research's economic and market forecasts for 2022 with Outlook 2022: Passing the Baton.

Source: WEEKLY COMMENTARY

Since we began our investing careers, we’ve had the concept of diversification drilled into our heads. Some refer to it as the only free lunch in investing. Well, when it comes to geography, that advice hasn’t been helpful for some time (you could say the same about value-style investing). Staying close to home and favoring the United States won’t always be the best move, but for now, we think it still is—as we discuss here.

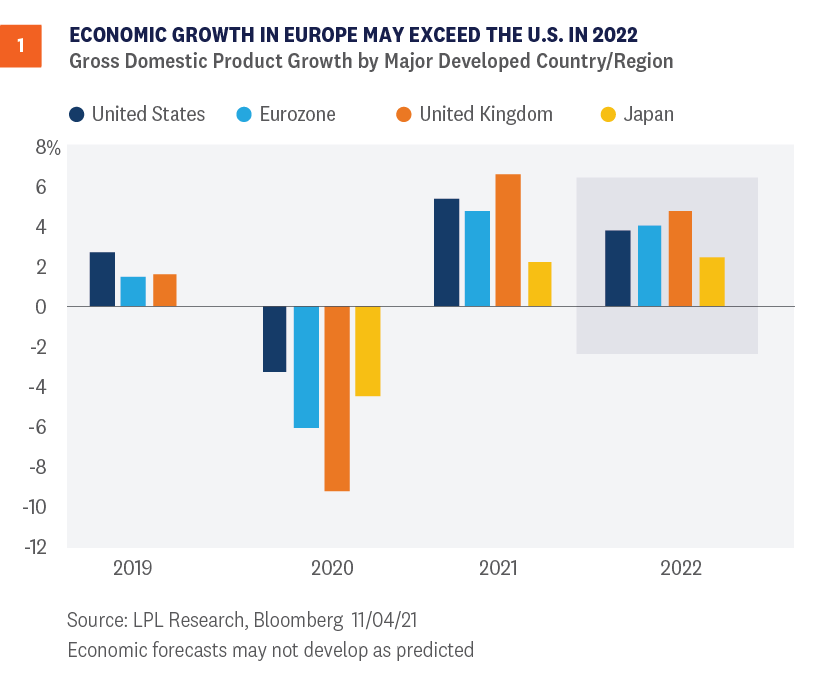

Europe’s Economy Showing Solid Improvement

It’s been difficult to find a macroeconomic story that supports reducing exposure to U.S. equities in favor of their developed international counterparts. But frankly, if one is going to develop, it may need to happen soon. As COVID-19 cases have fallen globally in recent months, it sets up a potentially synchronized global expansion in 2022. If that global expansion is accompanied by a weaker U.S. dollar and value stocks can at least hold their own, then we think developed international equities could be in a fairly good position to potentially outperform U.S. equities. As shown in Figure 1, the consensus forecasts for gross domestic product (GDP) growth in 2022 are calling for the European economies (the Eurozone and the United Kingdom) to grow faster than the United States next year. Europe and Japan are both ahead of the United States right now in vaccinations administered as a percentage of their populations (source: Ourworldindata.org), after playing some catch-up, which positions those economies to take the next step forward in their recoveries. Europe and Japan are also earlier in their economic cycles, leaving more upside in terms of growth potential. Forecasts for economic growth in Europe do look a bit better on a relative basis next year, and economic growth expectations for the second half of 2021 have held up relatively well recently despite the COVID-19 Delta variant wave, based on Bloomberg’s consensus GDP forecasts. However, Europe’s economic momentum may be peaking based on purchasing managers’ index data. Moreover, the Citi Economic Surprise Index for Europe stands at -51.5, compared to the one-year average of +90. In other words, European economic data has been mostly falling short of expectations and even missing more frequently than the U.S., where the surprise index reading is -20.5. Japan’s surprise index is also weak at -79. With solid economic growth expected in Europe, perhaps even slightly better than in the U.S., a neutral view (or market weight) has solid support. But with momentum in Europe likely past its peak and growth in Japan lagging behind, the case for a more positive view of international equities is not particularly compelling.

International Earnings Look Good, But So Does The U.S.

Similar to the economic growth picture, earnings are recovering nicely in Europe and Japan, but they don’t stand out relative to the United States. As major global economies recover from the pandemic, MSCI EAFE Index earnings are poised to grow nearly 50% in 2021, though that is only a few percentage points better than the U.S., based on the latest consensus estimates from FactSet (and those are just estimates at this point). Estimate revisions have been more positive in the U.S. than internationally, indicative of better earnings momentum and offsetting the attraction of the extra bit of earnings growth potential. So, at this point we’ll call earnings a toss-up, though perhaps the U.S. has a slight edge given its track record of surpassing expectations and heavy exposure to technology, e-commerce, and digital media.

Waiting For Value Stocks To Have Their Day

Perhaps the biggest problem for international equities right now in their more than decade-long struggles to keep up with the United States is the leadership of growth-style equities. Over the last 10 years, the Russell 1000 Growth Index has outpaced its Value counterpart by about 6.5 percentage points per year, while the MSCI EAFE has lagged the S&P 500 Index by about 8 percentage points per year. The MSCI EAFE Index for non-US developed market equities has only a 10% weighting in the technology sector, compared with 28% in the S&P 500, making it very difficult for developed international equities to keep up with the U.S. in a growth-led market. Add in internet retail and digital media, and the gap between these two markets gets even bigger. We believe a pickup in economic growth globally over the next quarter or two will help value stocks at least match returns for the growth style, with cyclically oriented value stocks potentially doing even a little better—a key ingredient for developed international equities’ prospects. But as long as U.S. growth stocks are leading, developed international will have a very difficult time keeping up over any meaningful period.

Technical Trends Stay With The U.S.

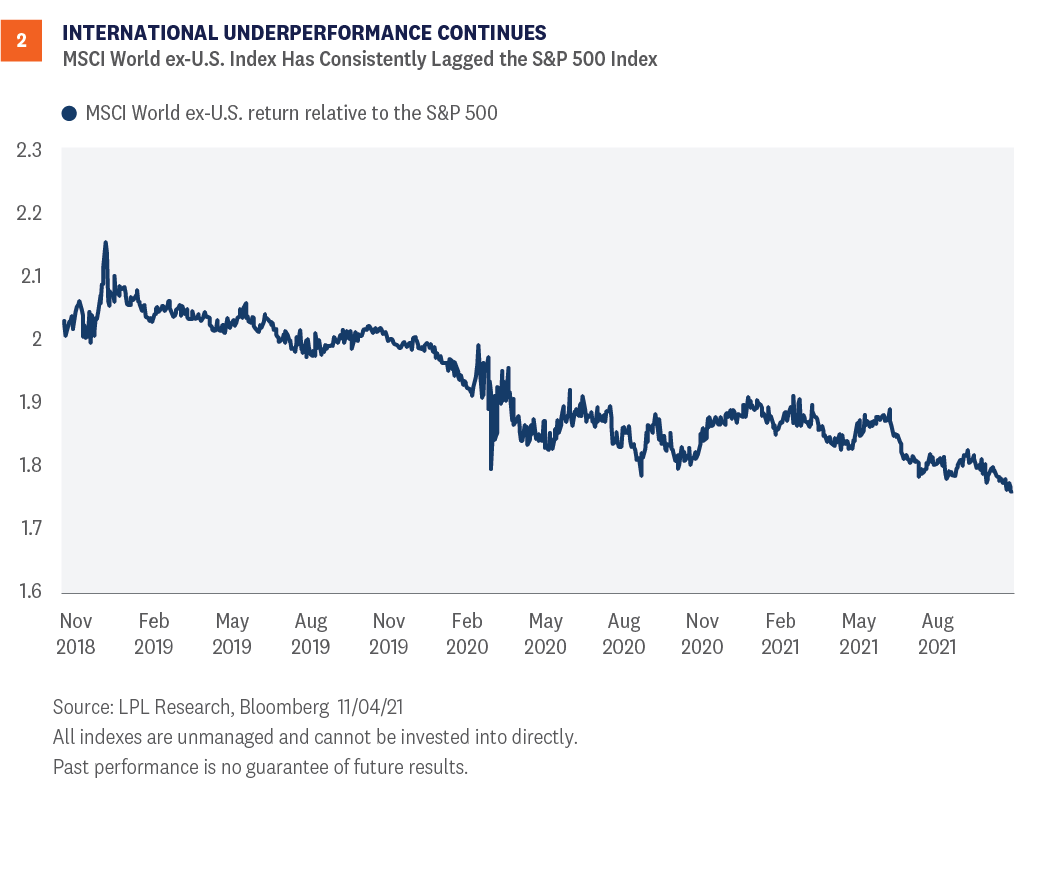

The technicals for international equities also support an overall cautious stance. As shown in Figure 2, the MSCI World Ex-U.S. Index, an index that incorporates both foreign developed and emerging markets, has continued to substantially lag the S&P 500, continuing the relative downtrend that had been in place prior to the pandemic. Dollar strength in 2021 is one reason for this, with the U.S. Dollar Index up more than 5% so far this year. Dollar strength hurts internationally diversified U.S. investors, as the currencies they are holding weaken relative to the dollar. However, even accounting for currency effects, international markets have steadily underperformed their U.S. counterparts, with China being one of the biggest culprits. China’s substantial weight in diversified emerging markets indexes is the primary reason the asset class has posted a slight loss so far this year. Looking forward, we see modest signs of technical improvement in China and international markets, but the accompanying chart shows the significant opportunity cost relative to the U.S., and would likely need to show some technical improvement, combined with an abatement of dollar strength, for us to consider a positive view of developed international (or overweight), or to reconsider our underweight recommendation for emerging markets.

Still Looks Like a Value trap

One of the most popular arguments in favor of investing in developed international equities has been valuations. Based on forward price-to-earnings ratios (PE), the MSCI EAFE Index is trading at a 27% discount to the S&P 500—the largest in the past 20 years and much larger than the average long-term discount of 9%. But stocks in Europe and Japan have been cheap for a long time, and it hasn’t helped relative performance. Valuations generally don’t tell us much about the next year or two, so we would need more reasons to re-allocate from U.S. equities to international than just low PE ratios. However, lower valuations have historically been well correlated with long-term returns, suggesting strategic investors who are in it for the long haul may benefit from international equity allocations.

Conclusion

If developed international market equities are going to outperform, we’re probably getting close to the point in time where we start to see it. Markets may be on the cusp of another rotation to value as global growth picks up, while economic growth in Europe, the majority of the MSCI EAFE Index, may exceed that of the U.S. next year. However, we still favor the U.S. over developed international markets as we enter 2022—primarily due to technical factors, including the weak momentum for the major stock indexes outside the U.S., the strong U.S. dollar, and continued strength in U.S. growth stocks, which makes it hard for the more value-oriented markets in Europe and Japan to keep up. For developed international markets, neither economic growth nor earnings stand out relative to the U.S., so sticking with what’s been working makes sense. Finally, our emerging markets equities recommendation remains negative due to ongoing regulatory risks in China, which could slow the growth of the Chinese economy and earnings, while also increasing uncertainty. Jeffrey Buchbinder, CFA, Equity Strategist, LPL Financial

Scott Brown, CMT, Senior Analyst, LPL Financial ______________________________________________________________________________________________ IMPORTANT DISCLOSURES This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy. U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio. All index data from FactSet. This research material has been prepared by LPL Financial LLC. Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity. Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-947201-1121| For Public Use | Tracking # 1-05209658 (Exp. 11/22)

We have used most of the superlatives we know to describe corporate America’s stunning performances over the past two earnings seasons. Despite lofty expections, results exceeded estimates by the biggest margins we’ve ever seen (and one of the authors of this report has been doing this for 23 years). We expect solid earnings gains during the upcoming third-quarter earnings season, but upside surprises will be smaller. Unfortunately, we won’t need as many superlatives.

Look for Many—But Smaller—Upside Surprises

Earnings growth in the first half of 2021 was amazingly strong, with S&P 500 Index earnings growing 52% and 90% year over year in the first and second quarters, shown in Figure 1. The growth was stellar, but the most impressive thing to us about these numbers was the more than 20 percentage point upside surprises for both quarters. Those surprises came after the bar had already been raised following strong earnings results during the second half of 2020. After being pleasantly surprised by corporate America for a year now, we won’t totally dismiss the possibility of big upside surprises again during the third-quarter earnings season. However, we would point to several reasons we think earnings growth overall will be much closer to the current third-quarter consensus estimate implying a 29% increase:

Slower economic growth from the Delta variant. According to the Federal Reserve Bank of Atlanta’s estimate, the growth rate of gross domestic product (GDP) for the third quarter is tracking to just 1.3%, down from 6% two months ago. Manufacturing demand remains robust based on new orders, but company surveys and anecdotes continue to point to difficulty filling those orders due to the supply chain disruptions.

Supply chain challenges have intensified. We have heard from a number of global companies in recent weeks that their profit margins are coming under more pressure from supply chain challenges. Nike cited shipping delays and factory shutdowns in Vietnam for lowering its guidance. FedEx lowered guidance amid rising labor costs, staffing shortages, and logistical challenges. Sherwin-Williams cut its outlook, citing materials shortages and higher-than-expected input cost inflation, exacerbated by Hurricane Ida. Margin pressures from shortages of labor and materials will be a common theme for the third quarter—and likely a quarter or two beyond.

Pre-announcement numbers are good, but not quite up to second quarter levels. The number of S&P 500 companies providing positive guidance for the third quarter has decreased by 11 compared to the second quarter, according to FactSet. Meanwhile, the number of companies providing negative guidance for the third quarter has increased by 10 compared with the second quarter. Still, more companies have provided positive guidance than negative guidance for five straight quarters for the first time in at least 15 years, which signals more than just a few percentage points of upside surprise to the S&P 500 earnings estimate.

Smaller increase in the consensus estimate. The estimate for third-quarter earnings rose during the quarter, but not as much as it did leading up to first- and second-quarter earnings seasons. The consensus third-quarter S&P 500 earnings estimate rose 2.9% over the three months ending September, down from increases of 7.2% for second-quarter earnings in the second quarter, and 6.5% for first-quarter earnings during the first quarter. Any increase is good, however, given the long-term average is a declineof 5%.

Bottom line—expect upside as earnings continue to benefit from the reopening and high profit margins. But don’t expect the massive upside surprises of recent quarters. A third-quarter earnings growth rate in the mid-to-high 30s would be excellent.

What We're Watching

Here are three things we will be watching as the numbers roll in and companies share thoughts about the future:

How long might supply chain issues last? It will be very interesting to hear how long companies expect supply chain bottlenecks and shortages of labor and materials to last. These pressures on companies’ costs may impair profit margins for the rest of 2021—and likely into 2022. Raising prices will help, but unfilled orders may cap revenue growth, making it difficult for companies to beat analysts’ earnings targets.

What is the outlook for wage increases? Wages are a big component of corporate America’s cost structure. We will be looking for confidence from companies that wage pressures will not get much stronger, though we anticipate higher wages will eat into profit margins in coming quarters. The question is how much. Productivity gains from technology investments (i.e., doing more with less) can only go so far in containing wage increases, which are already running above 4% annualized.

How will stocks react to smaller upside surprises? Investors and analysts may have gotten spoiled by massive upside surprises in recent quarters. We’re interested to see how the market will react to smaller beats and guidance that may not be enough to push analysts’ estimates materially higher. While most companies will clear the higher bar, few will soar well above it as so many did last quarter.

Conclusion

Earnings growth in the third quarter will likely be quite strong, possibly making a run at 40%. While that’s excellent growth, it’s a far cry from the 90% increase in S&P 500 earnings in the second quarter. It will be interesting to see how corporate America wades through supply chain issues. If those headwinds are continuing to intensify, then our $205 estimate for 2021 S&P 500 earnings will be tough to reach (FactSet’s consensus estimate is currently $201). Against this more challenging earnings backdrop, we maintain our positive stock market outlook. In the near term, we continue to look for dips to buy, given the prospects for a pickup in economic growth in the fourth quarter, still low interest rates, and historically strong fourth-quarter returns. Risks include another COVID-19 wave, stubbornly “sticky” inflation that could push interest rates sharply higher, potential tax increases in 2022, and, as always, geopolitics. Looking out to 2022, prospects for above-average economic growth and further earnings gains potentially point to another good year for stock investors, though probably not as good as 2021 has been. We expect interest rates to stay low enough to justify maintaining current valuations as earnings grow, which could set the stage for double-digit returns for the S&P 500 in 2022. More to come on our 2022 outlook in early December with the release of the yet-to-be-named Outlook 2022.

Jeff Buchbinder, CFA, Equity Strategist, LPL Financial

Ryan Detrick, CMT, Chief Market Strategist, LPL FinancialIMPORTANT DISCLOSURESThis material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy. US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio. All index data from FactSet. Please read the full Midyear Outlook 2021: Picking Up Speed publication for additional description and disclosure. This research material has been prepared by LPL Financial LLC. Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity. Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value RES-928450-1021 | For Public Use | Tracking # 1-05201962 (Exp. 10/22)

LPL Research Outlook 2022: Passing the Baton is designed to help you navigate the risks and opportunities over the rest of 2021 and beyond. While the economy continues to move forward, we’re still feeling some aftershocks of COVID-19 and the Delta variant. At the same time, 2021 also saw a resurgence of activities we missed in 2020, and the S&P 500 Index continued to advance as corporate America faced these challenges with resiliency. With the U.S. economy reopened, the growth rate may peak in second quarter 2021, but there is still plenty of momentum left to extend above-average growth into 2022. Inflation must be closely watched, but LPL Research believes recent price pressures are transitory, and that the strong economic recovery may continue to drive strong earnings growth and support further gains for stocks in the second half of 2021. The strong economic recovery and potentially higher inflation expectations may help push interest rates higher and lead to flat or potentially negative core bond returns in the second half. We’ve had a hand up that has helped us through a period of unique economic challenges. In 2022, the economy may be ready for a handoff, back to a greater emphasis on the individual choices of households and business. How smoothly that handoff is executed may determine the course of the recovery. LPL Research’s Outlook 2022 is here to provide insight on the economy, stocks, and bonds and what may lie ahead for next year and beyond.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. The economic forecasts may not develop as predicted. Please read the full Outlook 2022: Passing the Baton publication for additional description and disclosure. This research material has been prepared by LPL Financial LLC. Tracking #1-05207230 (Exp. 12/22)

With Halloween over the weekend, what better to write about this week than what scares us? If our positive near-term market outlook proves to be overly optimistic, we believe one—or perhaps more than one—of these five things will likely be the culprit: inflation, an aggressive Federal Reserve, profit margin pressures, pulling forward of seasonal gains, and potentially overly bullish sentiment.

Inflation

Central bankers are slowly acknowledging that inflation may be stickier than expected and that risks continue to tilt to the upside. At the same time, the baseline view remains that inflation will settle back toward historical norms over time. How long will that take? While inflation has come down some recently, we believe there may be another leg higher in the fourth quarter or early next year as the post-surge reopening pushes prices higher in areas where it had paused or declined as economic activity slowed, such as air fares, lodging, and used cars. The consensus expectation of Bloomberg-surveyed economists is that Consumer Price Index (CPI) year-trailing inflation will fall to 3.3% by the end of 2022 and 2.3% at the end of 2023. Many consumers, though, are finding inflation risks scarier, both due to sensitivity to prices in grocery stores and at the pump—and heavy news coverage. The wild card remains how long it will take supply chain disruptions to sort themselves out—they’ve been a key source of imbalances between supply and demand that have pushed prices higher. Also consider that the secular forces that put downward pressure on inflation for the past several decades (technology, “Amazon effect,” demographics, etc.) remain in place.

Aggressive Federal Reserve

Since March 2020, the Federal Reserve (Fed) has supported the economy and financial markets by purchasing $120 billion in U.S. Treasury and mortgage securities each month and keeping short-term interest rates near zero. As the economy continues to recover, however, the need for continued monetary support wanes. As such, the Fed is expected to fully end its bond buying programs by mid-2022 with interest rate hikes. In our view, this is likely coming in early 2023. The big wildcard remains how “sticky” inflation will be throughout 2022. As noted above, we think current inflationary pressures will abate over the next six to 12 months. However, if inflation is stickier than we are anticipating and the Fed is forced to aggressively respond early next year—first by potentially speeding up its tapering plans, and then by increasing short-term interest rates—economic growth will likely be negatively impacted. While we expect an orderly withdrawal of monetary support, an aggressive Fed reaction function to sustained inflationary pressures would likely spook financial markets.

Profit Margin Pressure

Third-quarter earnings results have been good overall. Companies have generally done an excellent job managing through supply chain disruptions, labor and materials shortages, and related cost pressures. Despite a high bar, a solid 82% of the roughly 280 S&P 500 companies that have reported have exceeded earnings targets. But there are reasons for concern. Profit margins are well above their pre-pandemic highs and carry downside risk. With labor in short supply (10.4 million job openings according to the Bureau of Labor Statistics, about 3 million above pre-pandemic levels), employers are having to pay up for talent. Wage growth accelerated to 4.6% year over year in September and will likely rise further—on top of the shortages of materials that push the prices up for manufacturers. These pressures on companies’ costs could impair profit margins if they continue to build. Consumers and businesses can afford to pay higher prices now but may balk at some point. For now, strong revenue growth is overshadowing these margin pressures but with stock valuations elevated, it’s important that earnings come through or markets may get spooked.

Seasonal Gains May Have Come Early

Stocks had one of their best Octobers ever, with the S&P 500 Index up more than 6% in the first month of the historically strong fourth quarter. But that’s the problem: October very well could have stolen some of the gains we usually see later in the year. The S&P 500 has historically gained 3.3%, on average, the final two months of the year. But, when the S&P 500 is up more than 5% in October, that average gain drops to 2.1% with a median of only 1.1%. After the year we’ve had, we don’t think anyone would have any issue with only modest additional upside through year-end, but we’d temper expectations on just how much green we could have the final two months. Some of the risks on this list could easily lead to another pullback like the one stocks experienced in September despite the generally positive economic and earnings backdrop.

Bullish Sentiment

We wrote last week about the bullish technical setup we see for equities in the final months of the year, and we believe the weight of the evidence supports that thesis. However, if there is a technical risk to watch, it is likely sentiment. The S&P 500 gained more than 6% in October following its first 5% pullback of the year, and as the saying goes, “nothing changes sentiment like price.” The percent of bulls in the American Association of Individual Investors (AAII) Investor Sentiment Survey more than doubled from its mid-September lows, while the VIX Index, a measure of implied volatility in the S&P 500 Index, is near its lowest level since before the pandemic began. Overall, we do not see evidence that sentiment is near extreme levels yet, or that the technical trends do not support a bullish view. But if the next few months do bring equity gains, sentiment may become a bigger risk. Conclusion

There you have it. Five things that scare us. That doesn’t mean there aren’t others (China anyone?). But if stocks suffer any meaningful volatility in the next couple of months, we think the culprit will likely be on this list. These potential scares do not, however, sway us from our positive near-term market outlook given prospects for a pickup in economic growth in the near term as COVID-19 cases decline. Stocks remain in a favorable seasonal period and low interest rates remain supportive. Stocks may also garner support from a potentially smaller-than-expected tax increase out of Washington, D.C. Ryan Detrick, CMT, Chief Market Strategist, LPL Financial

Jeffrey Buchbinder, CFA, Equity Strategist, LPL Financial

Barry Gilbert, PhD, CFA, Asset Allocation Strategist, LPL Financial

Lawrence Gillum, CFA, Fixed Income Strategist, LPL Financial ______________________________________________________________________________________________ IMPORTANT DISCLOSURES This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy. U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio. All index data from FactSet. This research material has been prepared by LPL Financial LLC. Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity. Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-942600-1021| For Public Use | Tracking # 1-05207404 (Exp. 11/22)

Last week, Congress was able to push back a fast-approaching deadline for raising the debt ceiling to December. Markets applauded the move with a relief rally. Despite decreased uncertainty in the near term, we may be confronted with the same problem again in a couple of months. This week we look more closely at the role the debt ceiling plays in government financing, what could happen if the debt ceiling is not raised in a timely way, and why market participants were skittish about the approaching deadline as we look ahead to December. Democrats and Republicans struck a deal last week to raise the debt ceiling, prompting a relief rally in equity markets. While failing to raise the debt ceiling was extremely unlikely, if it had happened it could have potentially done considerable damage to markets and the economy. But even approaching the deadline when the government would no longer be able to meet its obligations was having an impact. The mere appearance of Democrats and Republicans playing politics with the deadline was weighing on markets and forcing businesses to prepare for the very unlikely, but still possible, outcome of a government default. Unfortunately, we may have to do this all over again in December, and Congress does not yet seem to have fully learned from the 2011 debt-ceiling debacle that this issue is not to be taken lightly. Even if the current solution is just kicking the can for a couple of months, it does remove the immediate danger and opens up additional paths to address the problem well before the next deadline. The important debt-ceiling debate will continue, although with a reduced sense of urgency in the near term. In this Weekly Market Commentary, we take a closer look at the debt ceiling and the potential consequences of failing to raise it. 13 Questions Answered About the U.S. Debt Ceiling

1. What is the debt ceiling?

The debt ceiling is the limit on how much the federal government can borrow. Unlike every other democratic country (except Denmark), a limit on borrowing is set by statute in the U.S., which means Congress must raise the debt ceiling for additional borrowing to take place.

2. Why does the U.S. do it differently?

The debt ceiling was originally created to make borrowing easier by unifying a sprawling process for issuing debt to help fund U.S. participation in World War I. The process was further streamlined to help fund participation in World War II, creating the debt-ceiling process in use today. According to the Constitution, Congress is responsible for authorizing debt issuance, but there are many potential mechanisms that could make the process smoother.

3. Why is it important to raise the debt ceiling?

The government uses a combination of revenue, mostly through taxes, and additional borrowing to pay its current bills—including Social Security, Medicare, and military salaries—as well as the interest and principal on outstanding debt. If the debt ceiling isn’t raised, the government will not be able to meet all its current obligations and could default.

4. Has Congress always raised the debt ceiling?

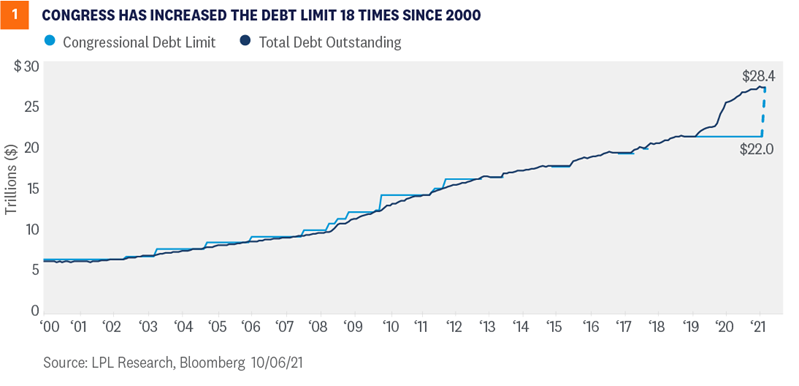

Yes, whenever needed. According to the Department of the Treasury (“Treasury”), since 1960 Congress has raised the debt ceiling in some form 79 times, 49 times under Republican presidents and 30 times under Democratic presidents. As shown in Figure 1, Congress has regularly raised the debt ceiling as needed. In fact, every president since Herbert Hoover has seen the debt ceiling raised during their administration.

5. Is the debt ceiling being raised to cover potential new spending programs?

No. Lifting the debt ceiling does not authorize any new spending. The debt ceiling needs to be raised to meet current obligations already authorized by Congress. Theoretically, not raising the debt ceiling would limit spending in the future, but only by deeply undermining the basic ability of the government to function, including funding the military, mailing out Social Security payments, and making interest and principal payments on its current debt. While perhaps symbolic of excessive spending, the debt ceiling is not the appropriate instrument to limit spending. Spending responsibility sits with Congress and the president, but Democrats and Republicans have both favored deficit-financed spending once in power. Bill Clinton’s presidency, much of it with a Republican Congress, was the only one that saw the publicly held national debt decline since Calvin Coolidge in the 1920s.

6. When was the debt ceiling last raised?

In August 2019 the debt ceiling was suspended for two years in a bipartisan budget deal and reinstated on August 1, 2021 at a level covering all borrowing to that date, the dashed line in Figure 1 representing the debt increase over that two-year period. Additional borrowing above the level that went into effect on August 1 has not been authorized.

7. If we were at the debt ceiling on August 1 and nothing happened, why is there a problem?

When we hit the debt ceiling, the Treasury is authorized to use “extraordinary measures” that allow the government to continue to temporarily meet its obligations, including suspending Treasury reinvestment in some retirement-related funds for government employees. The additional funding available through these measures is limited. Treasury Secretary Janet Yellen had said extraordinary measures would no longer be able to cover all government obligations as of October 18.

8. What’s the new deadline?

The recent increase in the debt ceiling will enable the government to meet its obligations through December 3, with maybe an additional few weeks from extraordinary measures, which have already been depleted.

9. Who won the debt ceiling battle?

Markets, the economy, and U.S. households and businesses. As for who won the battle politically—we leave to the politicians and voters.

10. What would the Treasury have to do if Congress failed to act in time?

Without the ability to issue new debt to pay existing claims, the Treasury would have to rely on current cash on hand and incoming cash, largely from taxes, to make its payments. So, the Treasury would be able to make some payments—just not all of them. As such, the Treasury department would likely have to prioritize its payments, although that could bring legal challenges. Moreover, the longer the delay in raising/suspending the debt ceiling, the harder it would be for the Treasury to make its payments. For a delay of a month for example, it is estimated that the Treasury department could only cover approximately 60% of its obligations. In that instance, severe spending cuts would likely be necessary. In 2011 and again in 2013, Federal Reserve and Treasury officials developed a plan in case the debt ceiling wasn’t addressed in time. At that time, they determined the “best” course of action would be to prioritize debt payments over payments to households, businesses, and state governments. By prioritizing Treasury debt obligations, it was assumed that the financial repercussions would be minimized. However, given recent comments by rating agencies (more on this below), there’s no guarantee that prioritizing debt payments would stave off severe, longer-term consequences like a debt downgrade or higher borrowing costs. Nonetheless, in order to adhere to the full faith and credit clause within the Constitution, debt-servicing costs would likely be prioritized.

11. U.S. Treasury debt was downgraded in August 2011 because Congress waited until the last minute to raise the debt ceiling. Could we see additional rating changes this time?

In August 2011, even though Congress acted before the U.S. was no longer able to meet all its obligations, one of the three main rating agencies, Standard & Poor’s (S&P), downgraded U.S. Treasury debt one notch from AAA to AA+. While the other two rating agencies retained the U.S. AAA rating, they both downgraded the outlook to negative. S&P has maintained that AA+ rating since 2011. Today, another of the three main rating agencies, Fitch, has threatened to downgrade U.S. debt if the debt ceiling isn’t raised or suspended in time. Further, Fitch has stated that prioritization of debt payments would lead to non-payment or delayed payment of other obligations “which would likely undermine the U.S.’s ‘AAA’ status.” So even if the Treasury made debt payments on time, the other obligations would be missed and likely result in a rating downgrade. Other rating agencies probably would follow suit as well. Another downgrade by a major rating agency may call into question use of Treasury securities as risk-free assets, which would have major financial implications globally. Of course, don’t forget that after the downgrade in August 2011, investors flocked to long-term U.S. Treasuries.

12. Could failure to address the debt ceiling push the economy into a recession?

It would depend on how long the Treasury would have to prioritize payments. If the delay is only a day or two, then it is unlikely the economy would slow enough to actually enter into a recession. Payments that were deferred would be repaid in arrears, so the economic impact would likely be minimal. However, if payment prioritization is necessary over a prolonged period of time—say a month or longer—this could indeed cause economic activity to contract. Since the government is running a fiscal deficit of around 7% of gross domestic product, and the Treasury could not issue debt to cover that deficit, spending cuts would need to take place. In that scenario, according to analysis by Oxford Economics, $1.5 trillion of spending would need to be cut. The spending cuts, if prolonged, would likely push the U.S. economy into recession. Moreover, the unknown knock-on effects, such as the impact on business confidence, would also likely slow economic growth.

13. How would a technical default impact the financial markets?

In 2011, which is probably the closest comparison to this year, the S&P 500 Index fell by over 16% in the span of 21 days due to the debt-ceiling debate and subsequent rating downgrade. The equity market ended the year roughly flat, so investors who were able to invest after that large drawdown were rewarded. However, that large drawdown was due solely to the policy mistake of not raising the debt ceiling in a timely manner. It’s likely that if Congress were to wait until the last minute again before raising or suspending the debt ceiling, equity markets would react similarly. Despite the downgrade, demand for intermediate and longer-term Treasuries actually picked up during the market volatility, pushing yields lower, as Treasuries are generally considered a “safe haven” asset. While that may have been the market reaction in 2011, there is no guarantee that, in the event of a technical default and further rating downgrades, Treasury securities would have a positive return this time around—particularly if Treasury securities lose their reputation as bonds that have no default risk.

Conclusion

Given the experience from 2011, we think it was prudent for Congress to raise the debt ceiling reasonably in advance of the October 18 deadline when the government would likely no longer be able to meet all its obligations. Political brinksmanship with the debt ceiling is a dangerous game, with likely relatively little to gain and much to lose. Despite the extension, the legislative agenda for the fourth quarter remains packed, we may run into the same problem again in December, and both parties are similarly motivated. But the extra time does mean there is an easier path to addressing the debt ceiling through the budget reconciliation process if Democrats choose to use it. For now, the relief from even the unlikely possibility of a debt-ceiling crisis is welcome and markets are justifiably reassured. Barry Gilbert, PhD, CFA, Asset Allocation Strategist, LPL Financial